Full Report

The numbers behind KBR, Inc.: as-reported financial statements and company metrics for FY2021–FY2025, traced to the source filings, opened with the share-price history those statements have to justify. Every linked figure opens the exact page of the filing it was printed on, with the statement row highlighted. Amounts in US$ millions unless noted.

Reading notes: Fiscal-year labels follow KBR's own convention: KBR uses a 52/53-week fiscal year ending on the Friday nearest December 31. FY2025 = year ended January 2, 2026; FY2024 = year ended January 3, 2025 (a 53-week year); FY2023 = year ended December 29, 2023. The corpus filenames and the numeric feed label these one year higher (e.g. the fiscal 2025 10-K is filed as 'KBR_annual_report_FY2026'); the numeric feed also carries a duplicate FY2024 entry equal to the year ended January 3, 2025. FY2023–FY2025 income-statement, cash-flow and backlog figures are presented on a continuing-operations basis after HomeSafe was reclassified to discontinued operations in fiscal 2025 (fiscal 2025 10-K). FY2021–FY2022 include the businesses now in discontinued operations. FY2024 revenue as originally filed was $7,742M (recast to $7,710M). Revenue-by-segment: KBR realigned its reportable segments effective fiscal 2025 — the former 'Government Solutions' segment was renamed 'Mission Technology Solutions' and the international business was redistributed into both segments; all periods in the fiscal 2025 10-K (FY2023–FY2025) were recast. FY2021–FY2022 are shown on the former Government Solutions / Sustainable Technology Solutions basis (International revenue was reported within Government Solutions), so the FY2022→FY2023 change in each segment partly reflects this redistribution rather than organic movement. MTS business-unit detail (Science and Space, Defense and Intel, Readiness and Sustainment) is shown only for the recast FY2023–FY2025 years. FY2021–FY2022 income-statement and per-share figures reflect the full-retrospective adoption of ASU 2020-06 (convertible notes) as presented in the fiscal 2022 10-K; balance-sheet FY2021 is cited from the same 10-K's comparative column.

Share Price — Full Available History — 20 Years

The stock closed at $35.17 on Jul 17, 2026 — up 69% over the window shown (+2.7% a year), trading between $9.86 and $72.02. At that close the stock trades at 11× FY2025 diluted EPS as reported below.

Source: market price feed, monthly closes, sampled from 4,945 source observations, Nov 2006–Jul 2026. Price return only, excludes dividends.

FY2025 at a Glance

Revenue (US$ millions)

Operating income (US$ millions)

Net income (US$ millions)

Diluted EPS

Source: FY2025 consolidated statements [1] [2]. Click any linked figure to open the filing page with the row highlighted.

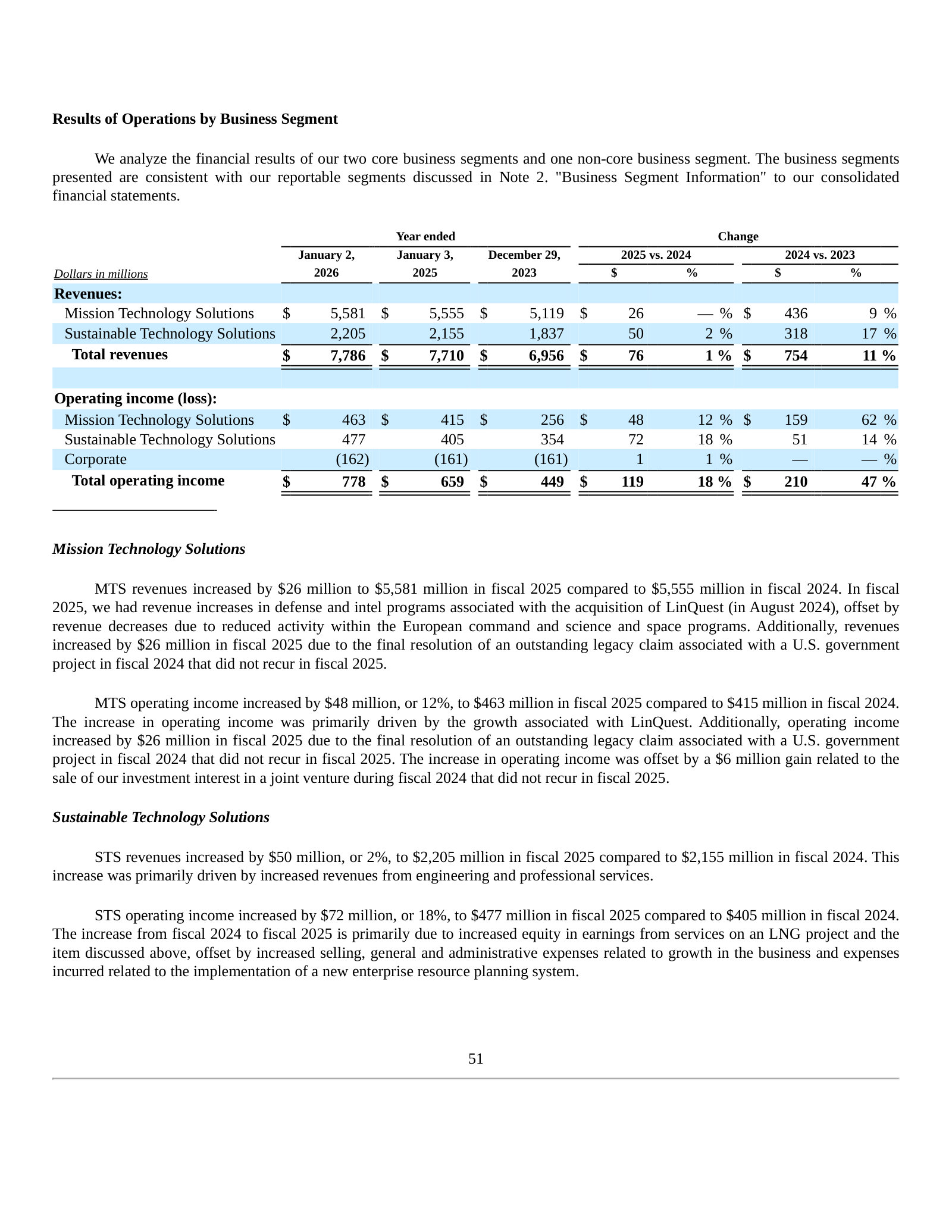

Revenue by Reportable Segment

| Revenue by Reportable Segment | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Mission Technology Solutions | 6,149 | 5,320 | 5,119 | 5,555 | 5,581 |

| Science and Space | — | — | 1,127 | 1,188 | 1,126 |

| Defense and Intel | — | — | 2,497 | 2,887 | 3,178 |

| Readiness and Sustainment | — | — | 1,495 | 1,480 | 1,277 |

| Sustainable Technology Solutions | 1,190 | 1,244 | 1,837 | 2,155 | 2,205 |

| Total revenues | 7,339 | 6,564 | 6,956 | 7,710 | 7,786 |

| Total revenues growth, derived | — | -10.6% | +6.0% | +10.8% | +1.0% |

Source: Form 10-K MD&A Results of Operations by Business Segment; Note 3 Revenue disaggregation (business-unit detail, recast FY2023–FY2025) [3] [4] [5]. Click any linked figure to open the filing page with the row highlighted.

Operating Income by Segment

| Operating Income by Segment | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Mission Technology Solutions | 414 | 441 | 256 | 415 | 463 |

| Sustainable Technology Solutions | (30) | 47 | 354 | 405 | 477 |

| Corporate | (153) | (145) | (161) | (161) | (162) |

| Total operating income | 231 | 343 | 449 | 659 | 778 |

Source: Form 10-K MD&A Results of Operations by Business Segment [4] [5]. Click any linked figure to open the filing page with the row highlighted.

Income Statement

Source: Consolidated Statements of Operations [1] [2]. Click any linked figure to open the filing page with the row highlighted.

Columns marked E are consensus analyst estimates shown alongside reported results for direct comparison; they are not company guidance.

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-17. Estimate figures link to the consensus source, not to filing pages.

Balance Sheet

Source: Consolidated Balance Sheets [6] [7] [8]. Click any linked figure to open the filing page with the row highlighted.

Cash Flow

Source: Consolidated Statements of Cash Flows (FY2023–FY2025 operating activities on a continuing-operations basis) [9] [10] [11]. Click any linked figure to open the filing page with the row highlighted.

Long-Term Record

| Fiscal year | Total revenue | Operating income | Net income (loss) attributable to KBR | Diluted earnings (loss) per share | Total cash flows provided by operating activities |

|---|---|---|---|---|---|

| FY2017 | 4,171 | 264 | 432 | 3.05 | 193 |

| FY2018 | 4,913 | 468 | 281 | 1.99 | 165 |

| FY2019 | 5,639 | 362 | 202 | 1.41 | 256 |

| FY2020 | 5,767 | 57 | (63) | (0.44) | 367 |

| FY2021 | 7,339 | 231 | 27 | 0.19 | 278 |

| FY2022 | 6,564 | 343 | 190 | 1.26 | 396 |

| FY2023 | 6,956 | 449 | (265) | (1.96) | 301 |

| FY2024 | 7,710 | 659 | 375 | 2.79 | 450 |

| FY2025 | 7,786 | 778 | 415 | 3.21 | 557 |

Source: consolidated statements across filings; older years from the standardized feed [9] [1] [11] [2]. Click any linked figure to open the filing page with the row highlighted.

Operating KPIs

| KPI | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Total backlog | 14,973 | 15,555 | 17,335 | 16,605 | 16,864 |

Source: company-reported operating metrics [12] [13] [14]. Click any linked figure to open the filing page with the row highlighted.

Analyst Consensus

Current price

Mean target

Median target

High target

Low target

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-17. Estimate figures link to the consensus source, not to filing pages.

Traceability

270 of 290 figures on this page (93%) link to the filing page where they are printed — click a linked figure to open the source PDF at that page with the row highlighted. Unlinked figures come from standardized data feeds or pre-filing years.

Fiscal-year labels follow KBR's own convention: KBR uses a 52/53-week fiscal year ending on the Friday nearest December 31. FY2025 = year ended January 2, 2026; FY2024 = year ended January 3, 2025 (a 53-week year); FY2023 = year ended December 29, 2023. The corpus filenames and the numeric feed label these one year higher (e.g. the fiscal 2025 10-K is filed as 'KBR_annual_report_FY2026'); the numeric feed also carries a duplicate FY2024 entry equal to the year ended January 3, 2025.

FY2023–FY2025 income-statement, cash-flow and backlog figures are presented on a continuing-operations basis after HomeSafe was reclassified to discontinued operations in fiscal 2025 (fiscal 2025 10-K). FY2021–FY2022 include the businesses now in discontinued operations. FY2024 revenue as originally filed was $7,742M (recast to $7,710M).

Revenue-by-segment: KBR realigned its reportable segments effective fiscal 2025 — the former 'Government Solutions' segment was renamed 'Mission Technology Solutions' and the international business was redistributed into both segments; all periods in the fiscal 2025 10-K (FY2023–FY2025) were recast. FY2021–FY2022 are shown on the former Government Solutions / Sustainable Technology Solutions basis (International revenue was reported within Government Solutions), so the FY2022→FY2023 change in each segment partly reflects this redistribution rather than organic movement. MTS business-unit detail (Science and Space, Defense and Intel, Readiness and Sustainment) is shown only for the recast FY2023–FY2025 years.

FY2021–FY2022 income-statement and per-share figures reflect the full-retrospective adoption of ASU 2020-06 (convertible notes) as presented in the fiscal 2022 10-K; balance-sheet FY2021 is cited from the same 10-K's comparative column.

Total backlog for FY2024–FY2025 excludes HomeSafe (discontinued operations); FY2021–FY2023 backlog includes it.

FY2017–FY2020 long-term-record figures are from the standardized SEC XBRL data feed and are shown without page links.

3 figure(s) differed between the data feed and the filing; the filing value is shown (see the run's metrics/metrics_tab.json for the audit trail).

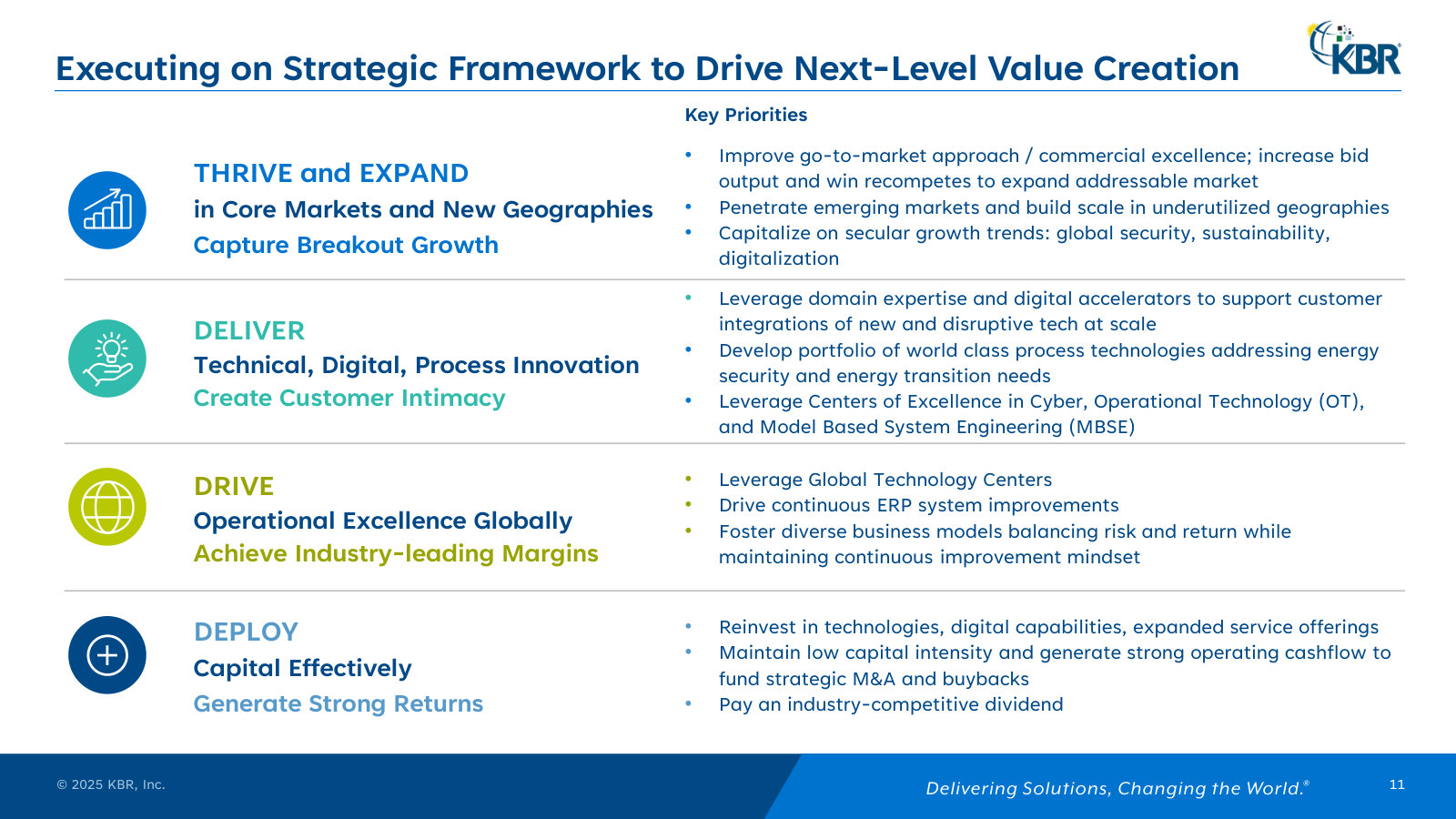

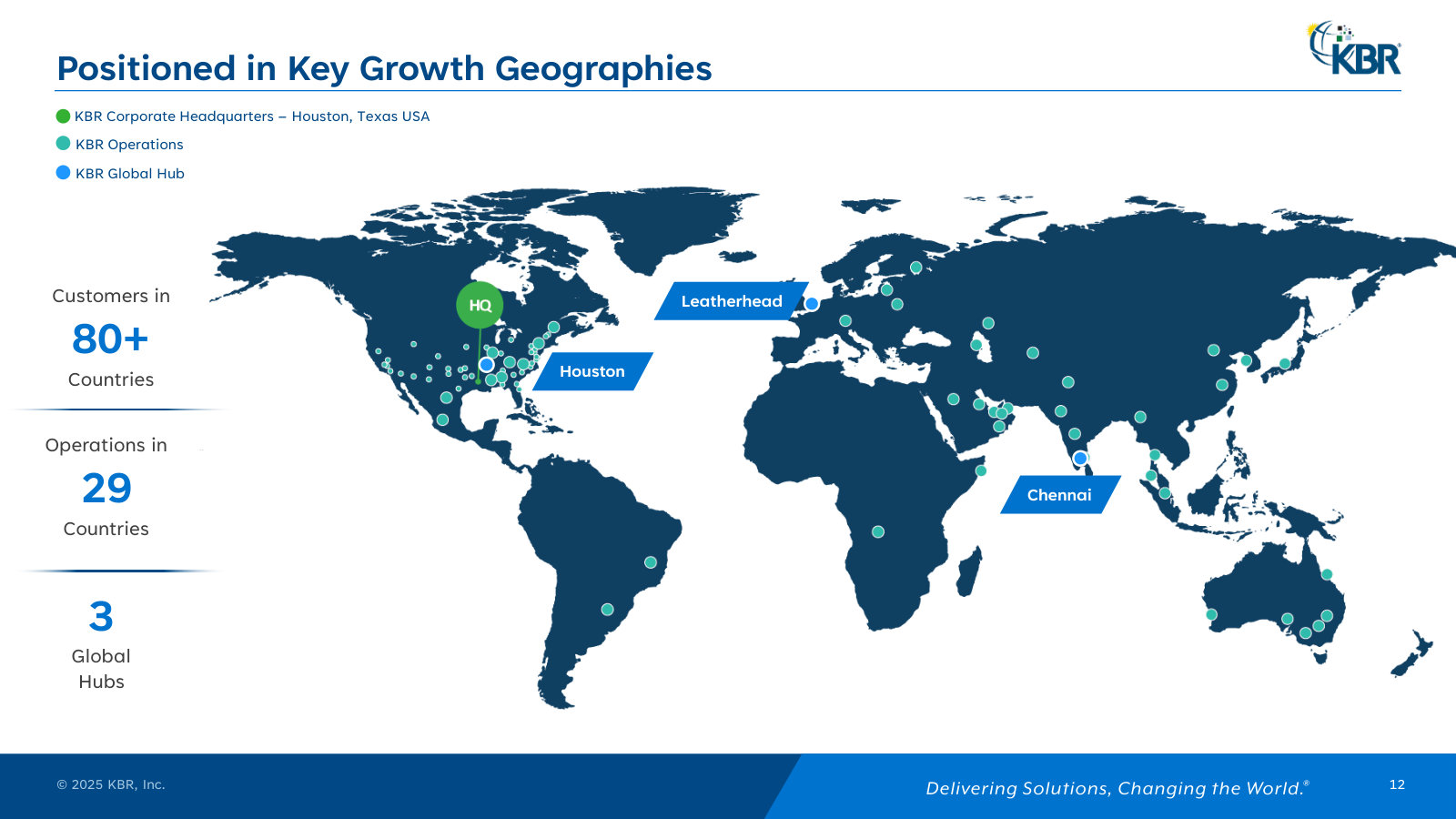

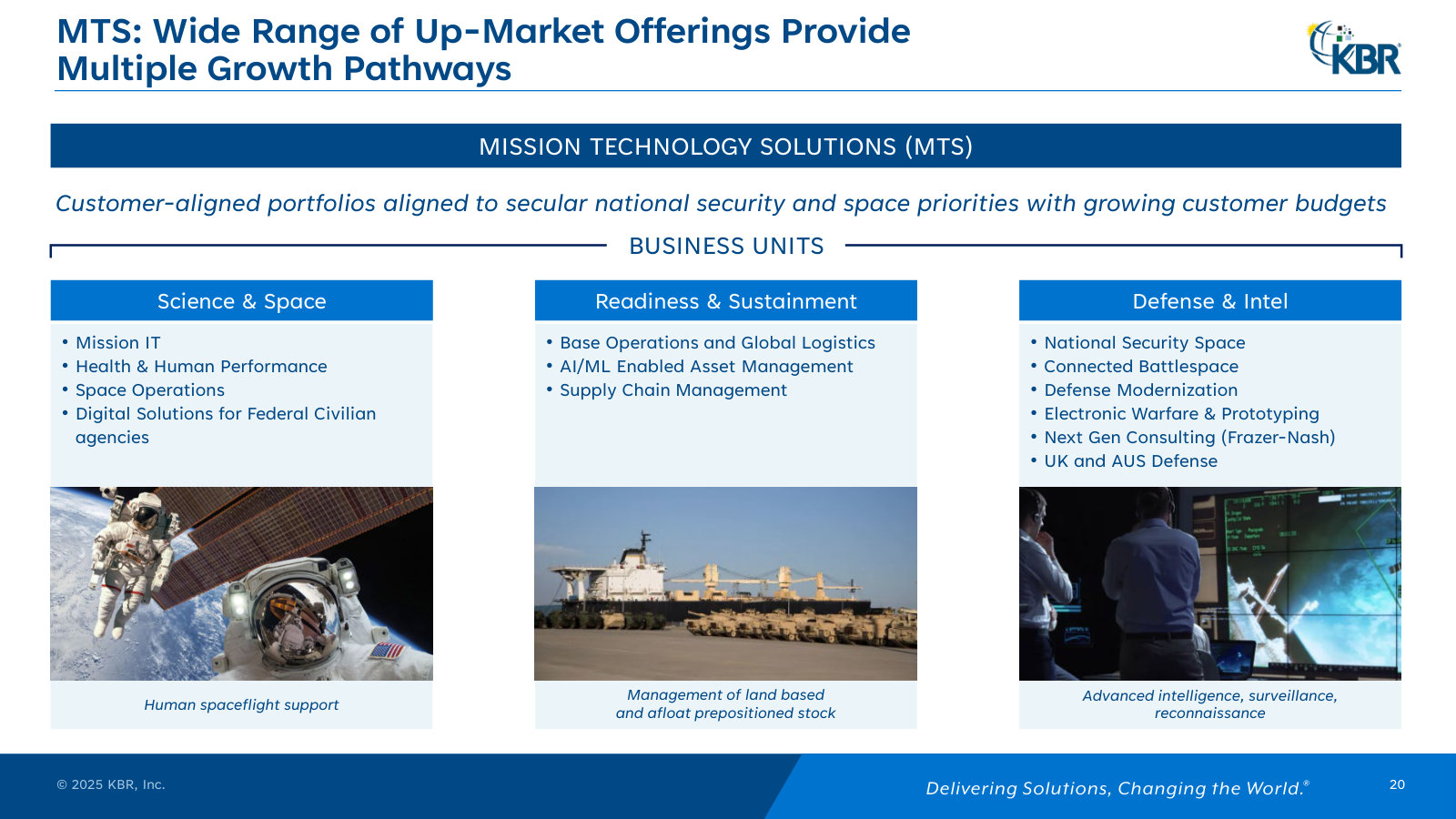

KBR, Inc.'s management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

Investor Presentation — July 2025 — July 2025

KBR's own company overview: what it does, its two segments, unit economics and strategy in one deck. Predates the 2026 spin-off. · Open the full document →

4Q & Full-Year 2025 Earnings Presentation — 4Q/FY2025

The latest full-year results and the headline event — KBR's planned tax-free split into two companies — with FY26 guidance. · Open the full document →

Investor Day 2024 — May 2024

The fullest strategy deep-dive — end-market sizing, segment pipelines and IP economics. Predates the MTS/STS rename; targets since revised. · Open the full document →

More from management

1Q 2026 Earnings Presentation — 1Q2026 · 27 pages · The latest quarter, and the updated spin-off timeline — separation now expected to close January 4, 2027. · Open →

4Q & Full-Year 2024 Earnings Presentation — 4Q/FY2024 · 27 pages · The prior full-year baseline — FY2024 actuals and guidance, before the spin-off narrative began. · Open →

KBR, Inc.'s management answers for the business every quarter. These are the exchanges that explain it best — verbatim, from the call transcripts preserved in Sources. Each link opens the full transcript at that page in a new tab.

Q1 FY2026 Earnings Call — Q1 FY2026

The most recent call: how STS earns its margins, the base rate ex-LNG, the two-company spin, and sizing the NASA risk. · Open the full transcript →

How STS earns its margins: a tier from technology licensing down to JV-accessed domestic maintenance.

Chad Evans, EVP & CFO: As shown on the left, you can see the margin tiering across the STS portfolio. Higher margins are driven by technology licensing and differentiated engineering while international OpEx services, PMC and proprietary equipment fit in the middle. At the lower end is domestic maintenance, which we primarily access through our recurring JV structure, allowing us to participate with appropriately managed risks and returns. As shown on the right, that mix supports a 20%-plus weighted STS margin profile in 2026 driven by technology, engineering and JV participation.

p. 5 · Read in context →

Why KBR is splitting itself: two pure-play companies as the culmination of a decade-long transformation.

Stuart Bradie, President & CEO: The strategic rationale for the separation remains unchanged. This spin reflects the culmination of a decade-long portfolio transformation and will result in two independent pure-play companies with clear strategic focus, distinct investment profiles and dedicated leadership aligned to their end markets. As part of this process, we evaluated all strategic alternatives and concluded that a spin is the right path to unlock value and position both businesses for long-term success.

p. 4 · Read in context →

The base STS margin is ~15% ex the LNG JV, with technology and licensing mix the lever above 20%.

Stuart Bradie, President & CEO: In the quarter, excluding that project, we made 16.1% as Chad referenced. The circa 15% that we put in that slide generally is the mark for the base business as we look forward ex that LNG project. […] There are margin expansion opportunities on mix, particularly around technology, where margins in that part of the business can be well in excess of 20%. The more we do in licensing and earlier-stage engineering, the better for margins.

p. 7 · Read in context →

Sizing the NASA in-sourcing risk that management flagged: $50-60M at most this year, likely less.

Stuart Bradie, President & CEO: The main comment on NASA relates to the new administrator's push for greater in-sourcing — effectively moving contractor staff back onto government payroll. That is being discussed and is being evaluated today. We think that may or may not happen over the next little while, but if it does, it will be gradual. We called that out on the call. In terms of scale to KBR, it's on the order of $50 million to $60 million through the course of the year in the most conservative read, and likely a lesser impact than that in practice.

p. 7 · Read in context →

Q4 & Full-Year 2025 Earnings Call — Q4 FY2025

The annual call: 2025 proof points and record cash return, the quality-of-earnings case in both segments, and whether MTS could be sold rather than spun. · Open the full transcript →

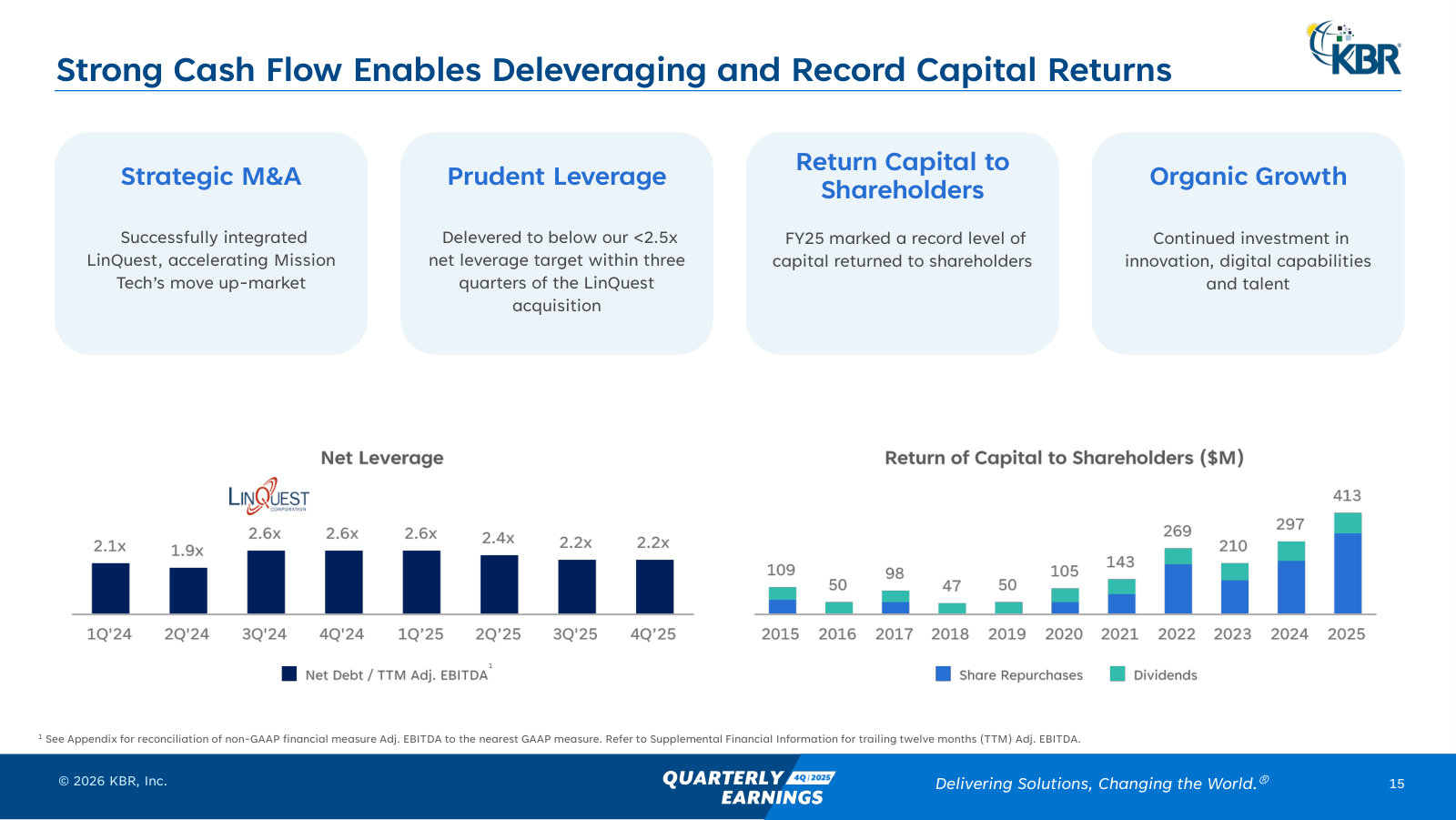

2025 proof points: margins up 100+ bps, 110% cash conversion, a record $413M returned, LinQuest integrated and debt paid down.

Stuart Bradie, CEO: Operational execution was a clear strength in 2025. We expanded margins by more than 100 basis points and generated operating cash flow with a conversion rate of 110%, delivering over $30 million in cost savings and expect this margin and cash performance momentum to continue into 2026. And finally, deploy capital effectively. We delivered $413 million in capital to shareholders in the year, and that's the highest in the last decade, successfully integrated LinQuest and delevered the balance sheet within a year.

p. 2 · Read in context →

The STS quality-of-earnings case: EBITDA up 16% since 2023, outpacing revenue, on track for 20%-plus margins by 2027.

Chad Evans, CFO: That operating discipline is clearly showing up in the quality of earnings. Adjusted EBITDA has grown 16% since 2023, outpacing revenue growth and reflecting improved mix and cost execution. While margins were modestly elevated in 2025, we are on pace to meet our long-term margin target of 20% plus in 2027.

p. 4 · Read in context →

How MTS lifted margin quality: fixed-price, technically differentiated work chosen for returns, not volume.

Chad Evans, CFO: Since 2023, the integration of LinQuest, strong international execution, and a more selective business development approach have supported mid-single-digit revenue growth while improving margin quality. Importantly, that improvement has been driven by commercial acumen and contract discipline, including a greater focus on fixed price and technically differentiated work, not volume. Even with near-term headwinds from award timing and process activity, the team remained highly selective in bids and recompetes, prioritizing returns and contract terms over scale.

p. 4 · Read in context →

Pressed on whether MTS could be sold instead of spun, Bradie will not rule out any value-enhancing approach.

Sangita Jain (KeyBanc); Stuart Bradie, CEO: My first one is, are you still exploring a sale of that segment? Can you speak to the process if you are? And is that still an option as you move towards the split? […] I cannot answer that question. However, we are committed to shareholder value, and that is absolutely true. We are currently going through this spin process to demonstrate our commitment. We are open to any approaches that could enhance shareholder value.

p. 8 · Read in context →

Q3 FY2025 Earnings Call — Q3 FY2025

The call after the September spin announcement: the transaction laid out, the shutdown-resilience thesis, how STS technology revenue and backlog actually work, and whether buyers have circled. · Open the full transcript →

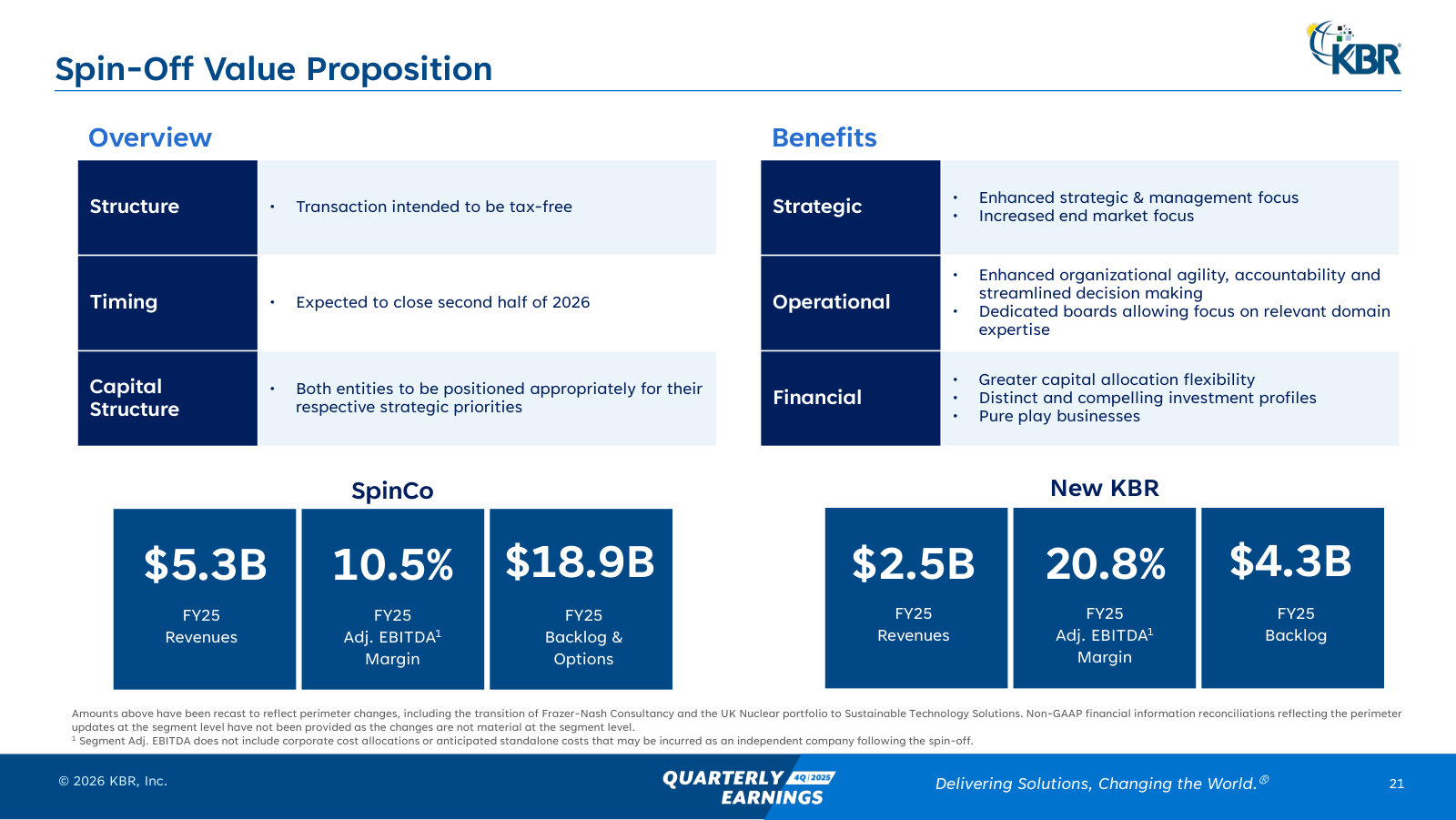

The spin, laid out: Mission Technologies becomes 'SpinCo,' New KBR keeps Sustainable Tech, two tax-free pure-play companies.

Stuart Bradie, CEO: Before the key takeaways, I will give you an update on the spin off, which was previously announced on September 24. We are spinning off our Mission Technologies segment, which I will refer to as SpinCo for now until a new name is announce later. New KBR will comprise the Sustainable Technology Solutions business. Our intent is to pursue this as a tax-free spin and upon completion of which KBR and its shareholders will benefit from ownership in two pure-play public companies with enhanced strategic focus, operational independence, and financial flexibility.

p. 4 · Read in context →

Why a U.S. government shutdown barely dents KBR: ~40% of revenue and 60%+ of EBITDA have zero federal-budget exposure.

Stuart Bradie, CEO: we'll remind you that circa 40% of KBR's group revenue and over 60% of adjusted EBITDA has zero exposure to the U.S. government spending budgets and of course, risk related to the shutdown. Within MTS U.S., the majority of our portfolio, as we've discussed many times, is comprised of mission essential operational work, many of which are well-funded multiyear programs. This provides short-term resilience to the government shutdown

p. 1 · Read in context →

How STS technology revenue breaks down: license fee, basic engineering, and lower-margin proprietary equipment, blended over time.

Stuart Bradie, CEO: Mark mentioned in his prepared remarks that this quarter we saw a significant amount of proprietary equipment reflected in the revenue. As we've discussed before, our technology sales consist of the license fee, basic engineering, and proprietary equipment. The overall combined margins align with our typical expectations; however, the proprietary equipment has a lower margin and there was an increase in that this quarter.

p. 9 · Read in context →

Why KBR reports STS backlog as a 6-8 month near-term figure rather than a headline total.

Stuart Bradie, CEO: If we looked at long-term backlog, the number would be so big that you wouldn't believe it, and rightly so because some of these projects go away. It's far better that we concentrate on what's real. For us, that sort of $5 billion or so in near-term backlog, which is 6 to 8 months.

p. 10 · Read in context →

Asked whether outside buyers have approached since the spin news, Bradie acknowledges inbounds but will not discuss them.

Tobey Sommer (Truist); Stuart Bradie, CEO: Could you tell us if you've received any interest from outside parties in acquiring either of the businesses since announcing the spin? […] Tobey, you know I can't answer that question. I'm sorry. I cannot answer that question. The thing that we have announced is going well in terms of under Mark's tutelage and is progressing as expected and on track. It is typical, I would say, that once you announce such things that you do get inbounds, but we are not at liberty to discuss them in any way, shape, or form, I'm sorry.

p. 8 · Read in context →

Q2 FY2024 Earnings Call — Q2 FY2024

Where the current shape was set: the LinQuest move into higher-end space and defense tech, the plan to collapse to two segments, and the ammonia technology moat. · Open the full transcript →

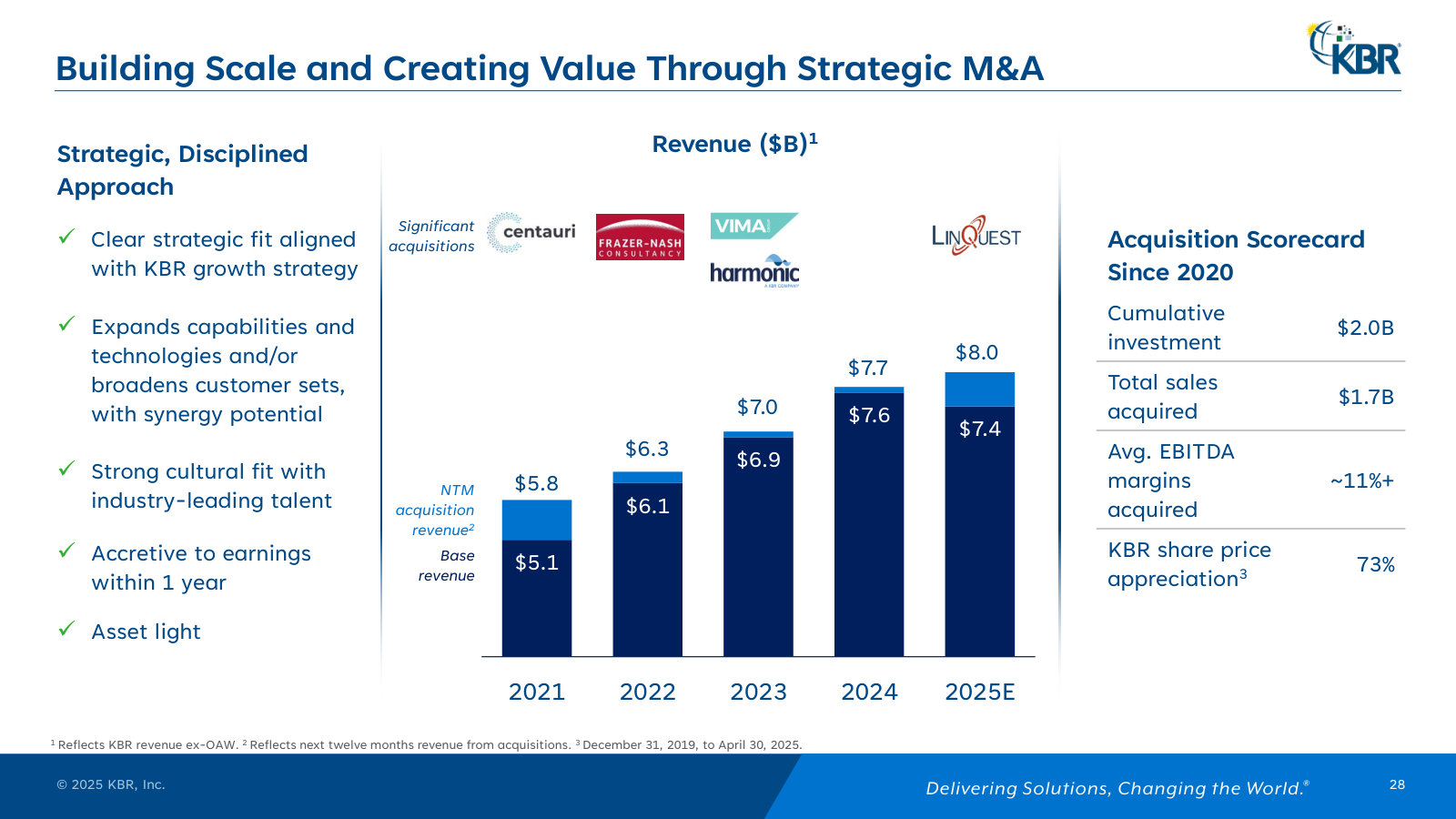

The LinQuest deal: 1,500 people in Space Force, JADC2 and national-security space, complementary with little overlap and double-digit margins.

Stuart Bradie, CEO: LinQuest has over 1,500 people. They do amazing work across National Security Space—think Space Force, Future Air Dominance, the Air Force, and JADC 2—and connected battlespace, meaning interoperability and digital. Their capability is highly complementary to KBR’s with little overlap, which I think gives exciting synergy opportunities. We've highlighted how those work on the slide. We're also excited about the fact that they have double-digit margins as well as a robust presynergy growth profile, which is terrific.

p. 3 · Read in context →

Foreshadowing the two-segment structure: collapse three units to two, managed globally to cut complexity and capture synergies.

Stuart Bradie, CEO: Following these points from Investor Day, with LinQuest as a catalyst, we believe there are opportunities to realign our business to operate even better based on our capabilities and markets. The objective of this realignment will be to reduce complexity, realize synergies like AUKUS and One Saudi as we presented at Investor Day. We will likely manage both segments globally to allow for greater standardization and business process optimization, which should drive efficiency. We will work on this through the remainder of 2024 and expect to report results along these lines in full year 2025. To be clear, the segments and enterprise targets for 2027 will remain intact through this realignment.

p. 4 · Read in context →

How the realignment reshuffles work: the Diriyah Gate mega-project moves from Government into Sustainable Tech.

Stuart Bradie, CEO: We'll move from three business units to two effectively with bits of what we've been describing as GSI. I'll give you a good example: The Diriyah Gate project, which is a full-on project management of a new sustainable city in Saudi Arabia, currently sits in the government segment but could—given its commercial contractual basis, its program management at scale, and its location—realize our One Saudi vision by leveraging our position across our broader customer base. That sort of project will move into STS going forward.

p. 4 · Read in context →

STS's technology moat: the only two blue-ammonia projects worldwide to reach FID both run on KBR's proprietary process technology.

Stuart Bradie, CEO: In fact, there are only two blue ammonia projects in the world that have reached final investment decision, and both are using KBR's technology. These are the OCI plant in Bowman, Texas, and Fertiglobes in the UAE, which will make KBR's proprietary process technology the first to produce blue ammonia. This, in addition to our industry position in green ammonia, puts us in a very strong position.

p. 2 · Read in context →

More calls

Q2 FY2025 Earnings Call — Q2 FY2025 · 10 pages · For the mid-2025 picture under the new MTS/STS segments: tariff and Middle East headwinds, EUCOM step-down, and $21.6B backlog. · Open →

Q1 FY2025 Earnings Call — Q1 FY2025 · 11 pages · The first quarter reported under the new Mission Tech / Sustainable Tech segments, with record backlog going into the year. · Open →

Q4 & Full-Year 2024 Earnings Call — Q4 FY2024 · 14 pages · The FY2024 annual: the segment realignment completed, first full-year view with LinQuest, and ~$21B backlog. · Open →

Q3 FY2024 Earnings Call — Q3 FY2024 · 8 pages · LinQuest's first quarter inside KBR: integration progress and its lift to the Defense & Intelligence business. · Open →

Q1 FY2024 Earnings Call — Q1 FY2024 · 8 pages · The pre-transformation baseline: KBR before LinQuest and before the two-segment realignment, under the old Government Solutions structure. · Open →

KBR, Inc.'s annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

KBR, Inc. — Fiscal 2025 Annual Report (Form 10-K) — Fiscal 2025 (year ended Jan 2, 2026)

The year KBR recast itself: it renamed Government Solutions to Mission Technology Solutions and moved to spin it off into a separate public company. · Open the full document →

Item 1. Business — Company Overview — p. 12 · Read the full section →

How management defines KBR and its shift toward technology-driven, higher-return solutions for governments and commercial clients.

What KBR is and the operating-model shift management is steering in fiscal 2025.

KBR, Inc., a Delaware corporation ("KBR" or, the "Company"), delivers science, technology, engineering and logistics support solutions to the U.S. federal government, allied nations and commercial clients around the world. […] In the fiscal year ended January 2, 2026 ("fiscal 2025"), KBR’s operating model continued to shift toward agile, technology-driven, solutions-oriented delivery and was streamlined to increase strategic focus and to move upmarket into differentiated areas that we believe will provide attractive returns and consistent growth with favorable cash conversion.

p. 12 · Read in context →

Item 1. Business — Our Business Segments — p. 16 · Read the full section →

The two engines of revenue: defense/space mission services (MTS) and 85+ proprietary sustainability process technologies (STS).

The two core segments — Mission Technology Solutions and Sustainable Technology Solutions — in management's words.

Mission Technology Solutions. Our Mission Technology Solutions business segment provides full life-cycle support solutions to defense, intelligence, space, aviation and other programs and missions for military and other government agencies primarily in the U.S., U.K. and Australia. […] Sustainable Technology Solutions. Our Sustainable Technology Solutions business segment is anchored by our portfolio of over 85 innovative, proprietary, sustainability-focused process technologies that reduce emissions, increase efficiency and/or accelerate and enable energy transition across the industrial base in four primary verticals: ammonia/syngas, chemical/petrochemicals, clean refining and circular process/circular economy solutions.

p. 16 · Read in context →

Item 1. Business — Mission Technology Solutions Spin-off — p. 18 · Read the full section →

The defining strategic event: KBR intends to split its largest segment into a standalone public company, targeted for 2H fiscal 2026.

The planned tax-free spin-off of Mission Technology Solutions.

In September 2025, we announced our intention to spin off our Mission Technology Solutions business into a separate, U.S. publicly-traded company (the "Planned Spin-Off"). The Planned Spin-Off is intended to be tax-free to us and our shareholders for U.S. federal income tax purposes and targeting completion in the second half of the fiscal year ended January 1, 2027 ("fiscal 2026"). The spin-off will be subject to final approval by our Board of Directors and other customary conditions, including receipt of a favorable opinion of legal counsel and/or a private letter ruling from the U.S. Internal Revenue Service with respect to the tax treatment of the transaction for U.S. federal income tax purposes, the effectiveness of a registration statement on Form 10 filed with the SEC, satisfactory completion of financing and other regulatory approvals. Because the intended transaction is a spin-off, the Mission Technology Solutions business is not classified as held for sale and will be reported as continuing operations.

p. 18 · Read in context →

Item 1A. Risk Factors — p. 47 · Read the full section →

The two risks most specific to KBR: executing the spin-off, and dependence on government budgets — U.S. agencies alone are ~57% of revenue.

Revenue concentration in government spending that customers can modify or terminate at will.

Demand for our services provided under government contracts is directly affected by spending by our customers. […] We derive a significant portion of our revenues from contracts with agencies and departments of the U.S., the U.K. and Australia governments, which is directly affected by changes in government spending priorities and availability of adequate funding. […] The loss of work we perform for governments or decreases in governmental spending and outsourcing could have a material adverse effect on our business, results of operations and cash flows.

p. 55 · Read in context →

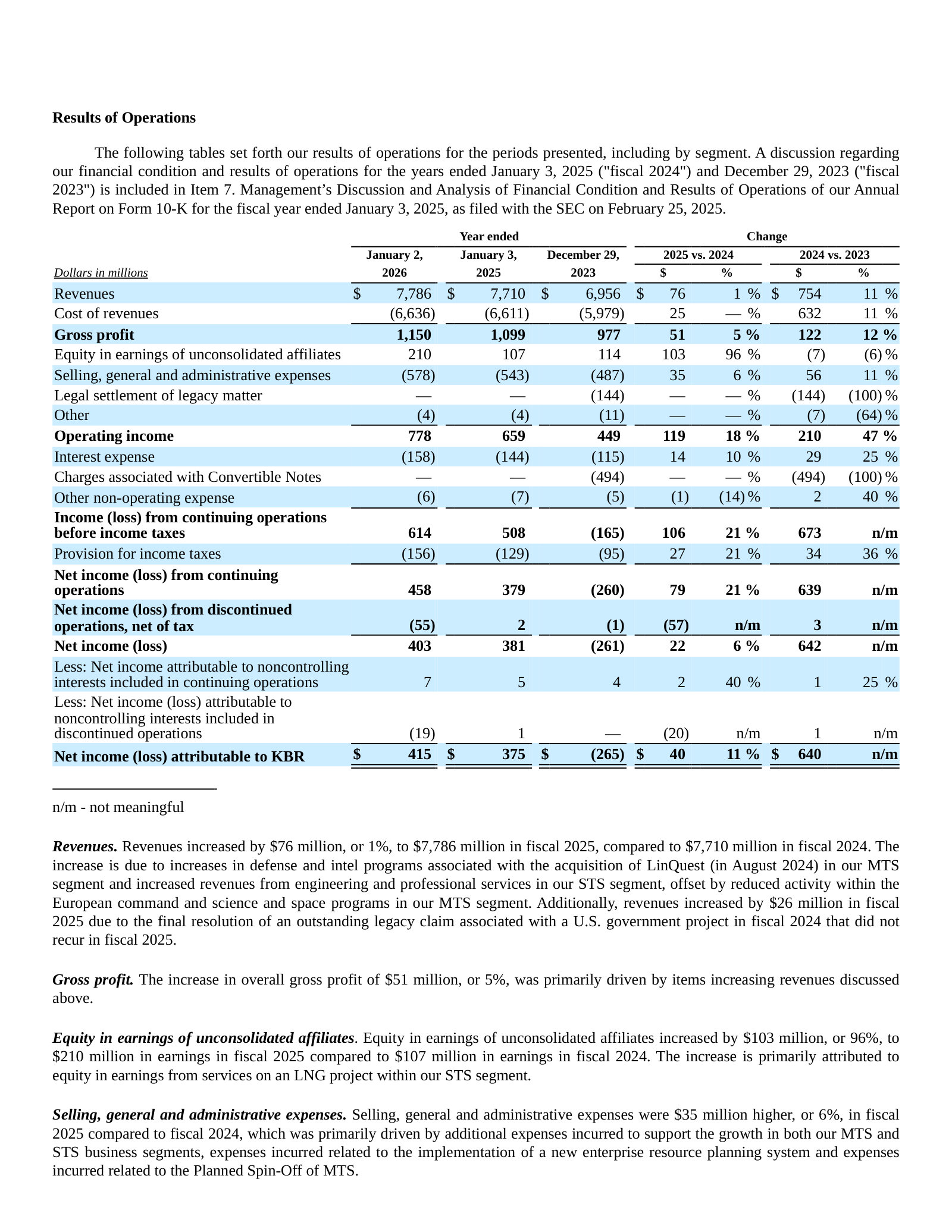

Item 7. MD&A — Results of Operations — p. 82 · Read the full section →

Revenue up 1% to $7,786M yet operating income up 18% to $778M — the margin and equity-earnings story management tells for fiscal 2025.

Item 7. MD&A — Results of Operations by Business Segment — p. 85 · Read the full section →

Segment economics: MTS $5,581M revenue / $463M operating income, STS $2,205M / $477M — STS the smaller, higher-margin engine.

What actually moved MTS revenue — LinQuest offset by European command and space program declines.

MTS revenues increased by $26 million to $5,581 million in fiscal 2025 compared to $5,555 million in fiscal 2024. In fiscal 2025, we had revenue increases in defense and intel programs associated with the acquisition of LinQuest (in August 2024), offset by revenue decreases due to reduced activity within the European command and science and space programs.

p. 85 · Read in context →

Item 7. MD&A — Critical Accounting Policies and Estimates — p. 97 · Read the full section →

The policy that defines a contractor's earnings: over-time revenue on the cost-to-cost method, driven by cost-to-complete estimates.

KBR, Inc. — Fiscal 2024 Annual Report (Form 10-K) — Fiscal 2024 (year ended Jan 3, 2025)

Included to show the segment before the recast: the same defense/space business was reported as 'Government Solutions,' a year before the rename and planned spin-off. · Open the full document →

Item 1. Business — Our Business Segments — p. 14 · Read the full section →

The prior-year name for today's Mission Technology Solutions — evidence of the fiscal-2025 rebrand and reorganization.

The segment reported as 'Government Solutions' in fiscal 2024, later renamed Mission Technology Solutions.

Government Solutions. Our Government Solutions business segment provides full life-cycle support solutions to defense, intelligence, space, aviation and other programs and missions for military and other government agencies primarily in the U.S., U.K. and Australia.

p. 14 · Read in context →

More annual reports

KBR, Inc. — Fiscal 2023 Annual Report (Form 10-K) — Fiscal 2023 (year ended Dec 29, 2023) · 142 pages · Pre-LinQuest, pre-spin-off baseline: $6,956M revenue with the legacy legal settlement and convertible-note charges booked that year. · Open →

KBR, Inc. — Fiscal 2022 Annual Report (Form 10-K) — Fiscal 2022 (year ended Dec 31, 2022) · 160 pages · Earlier Government Solutions / Sustainable Technology Solutions structure for multi-year trend comparison. · Open →

KBR, Inc. — Fiscal 2021 Annual Report (Form 10-K) — Fiscal 2021 (year ended Dec 31, 2021) · 181 pages · The earliest edition on hand, useful for tracing the pivot from legacy E&C toward government and technology services. · Open →

Competitors describe KBR, Inc.'s market in their own filings and calls. These verified passages and visual pages show where their strategies meet, using source documents preserved in Sources.

Leidos Holdings, Inc. (LDOS)

The largest U.S. government-services and defense-technology contractor, and KBR's most direct rival across defense systems, space, intelligence and IT modernization. Leidos names KBR by name in its 10-K competitor list.

Leidos's FY2025 10-K lists KBR among its named principal competitors across systems integration and defense engineering/technical services.

Our principal competitors currently include the following companies: Accenture Federal Services LLC, Amentum Services Inc., KBR, Inc., BAE Systems, Booz Allen Hamilton Inc., CACI International Inc., Deloitte, General Dynamics Corporation, GovCIO, IBM, KBR Inc., L3Harris Technologies, Inc., Lockheed Martin Corporation, ManTech, Northrop Grumman Corporation, Optum, Parsons Corporation, Peraton Inc., RTX Corporation and SAIC.

p. 11 · Read in context →

Leidos's CEO describes a defense-systems growth pivot spanning U.S., U.K. and Australia government programs — the international government footprint KBR also serves.

Thomas A. Bell (Chief Executive Officer): we're very bullish on our opportunity to help this administration increase the size and lethality of the U.S. Navy. And I'm very proud that both in Australia and the U.K., we have corollary unmanned autonomous vehicle programs that have synergy with what we're doing here in the U.S. So all in all, we see a tremendous pivot for our defense business […] now really pivoting to LRIP and programs of record, which has always been our plan since we acquired our defense tech business some years ago.

p. 5 · Read in context →

Leidos points to expanded NASA ARTEMIS space-program work and an international air-traffic-management win among recent government awards.

Thomas A. Bell (Chief Executive Officer): We are expanding our contribution under an asset contract to support the ARTEMIS program in long-duration space exploration. And we received a large award to modernize Kazakhstan's air traffic control system using our Skyline X comprehensive air traffic management system.

p. 1 · Read in context →

Science Applications International Corporation (SAIC)

A pure-play U.S. government technology integrator in defense, space, intelligence and civilian IT modernization — the closest listed analog to KBR's Government Solutions mission-IT and digital-engineering work.

SAIC frames its served market as the full-lifecycle U.S. government technical/engineering/IT space and sizes its footprint at roughly 1,700 active contracts and 23,000 employees.

As one of the largest pure-play technology service providers to the U.S. government, we serve markets of significant scale and opportunity. Our primary customers are the departments and agencies of the U.S. government. […] We serve our customers through approximately 1,700 active contracts and task orders and employ approximately 23,000 individuals

p. 45 · Read in context →

SAIC's CFO acknowledges nontraditional commercial entrants in the government market and defends SAIC's differentiated role as a “mission integrator.”

Prabu Natarajan (Chief Financial Officer): we are seeing new entrants in the market, nontraditional, with more commercial orientation to them. […] we welcome newcomers in the industry as a mission integrator. I think we believe sincerely that the offerings from commercial vendors still will require mission integration at its core to be able to operate inside of the government environment. So we welcome the competition in the industrial base.

p. 4 · Read in context →

SAIC discloses new-business win rates approaching 50% and recompete win rates of roughly 85–90% in its differentiated engineering and mission-IT work.

Prabhu Natarajan (Chief Financial Officer): our win rates on non-enterprise IT work—some of the work we do on the engineering side as well as the mission IT side—our win rates on new have approached 50% or more at various points over the last couple of years. […] our recompete win rates on non-commoditized enterprise IT is sort of in that 85% to 90% range. So good win rates outside of the commoditized enterprise IT work

p. 7 · Read in context →

Amentum Holdings, Inc. (AMTM)

A large government mission-and-engineering services contractor (defense, intelligence, space, nuclear/environmental) formed in part from Jacobs's former government business. Amentum names KBR by name as a primary competitor.

Amentum's FY2025 10-K lists KBR Inc. among its named primary competitors in U.S. government services.

Amentum's primary competitors include Booz Allen Hamilton Inc., CACI International Inc., KBR Inc., Leidos Holdings Inc., ManTech International Corporation, Parsons Corporation, Peraton Corporation, Science Applications International Corporation and V2X, Inc. Our domestic competition also includes large defense contractors such as Boeing Co., BAE Systems plc, General Dynamics Corporation, L3Harris Technologies Inc., Lockheed Martin Corporation, Northrop Grumman Corporation and RTX Corporation.

p. 10 · Read in context →

Amentum frames its addressable scope around C5ISR, space and digital modernization, cites a long-standing NASA space-operations franchise, and reports ~81% of revenue from direct U.S. Government contracts.

Our expertise is broadly applicable to many of the government's highest priority areas including command, control, communications, computer, combat systems, intelligence, surveillance and reconnaissance (collectively, "C5ISR"), RDT&E, energy, space, and digital modernization. […] our expertise in space operations, developed via our longstanding trusted relationship with NASA, which will help foster the development of next-generation civil and commercial space programs […] Approximately 81% of the Company's revenues were derived through direct contracts with agencies of the U.S. Government for the year ended October 3, 2025.

p. 6 · Read in context →

Amentum's CEO defines the company's core growth areas as intelligence operations, environmental remediation and defense engineering, logistics and modernization.

John Heller (Chief Executive Officer): Our core growth areas where we have long-standing leadership positions across large, stable, mission critical areas provide dependable revenue, strong cash flow, and predictable returns […] some notable areas include RDT&E, intelligence operations and analysis, homeland security and border protection, environmental remediation, and defense engineering, logistics, and modernization.

p. 3 · Read in context →

Technip Energies N.V. (TE)

A leading energy-transition engineering and process-technology licensor (LNG, hydrogen, ammonia, ethylene) that competes with KBR's Sustainable Technology Solutions segment — while also partnering with KBR in the KTJV joint venture on LNG.

Technip Energies names KBR as its partner in the KTJV joint venture selected for the Lake Charles LNG export project — a case where the two firms partner even as they compete elsewhere in process technology.

The KTJV joint-venture between Technip Energies and KBR has been chosen for a Major […] contingent on Lake Charles LNG's final investment decision.

p. 30 · Read in context →

Technip Energies claims the single largest installed base of on-purpose hydrogen plants of any engineering-and-technology company — a market KBR's clean-hydrogen licensing also targets.

the Group has delivered more than 275 hydrogen plants to its clients over the past 65 years, an estimated 30% of the installed base for on-purpose hydrogen, which represents the largest share of plants that a single engineering and technology company has delivered.

p. 16 · Read in context →

Technip Energies claims world leadership in polymer-resin and petrochemical process units, with more than 350 facilities delivered — overlapping KBR's petrochemicals and chemical-recycling licensing.

A world leader in the process design, engineering, procurement and construction of units for the production of polymer resins and other petrochemical derivatives, Technip Energies has delivered more than 350 facilities over the last 50 years.

p. 21 · Read in context →

Booz Allen Hamilton Holding Corporation (BAH)

The largest provider of technology consulting and analytics to U.S. defense and intelligence agencies, and the self-described largest AI provider to the federal government — the incumbent KBR contends with as it pushes AI and digital modernization into the same missions.

Booz Allen's FY2026 10-K claims the leading position in AI-for-government (about 400 active AI projects) alongside a top-tier federal/defense/intelligence cyber business.

As the federal government's largest AI provider with approximately 400 active AI projects, we build secure AI solutions and advanced capabilities spanning agentic AI, physical AI, and AI-Radio Access Network (AI-RAN), and other emerging technologies designed for mission critical environments. […] We also have one of the most impactful cyber businesses globally, protecting U.S. federal, defense, and intelligence agencies

p. 7 · Read in context →

Booz Allen's CEO frames its defense and intelligence (“national security”) portfolio as materially stronger than the civil sector and asserts leadership in cyber, AI and warfighting technologies.

Horacio Rozanski (Chairman, Chief Executive Officer and President): The conditions in our defense and intelligence sectors, broadly referred to as our national security portfolio, are fundamentally different and considerably stronger than those in the civil sector. […] our leadership in cybersecurity, AI, and war fighting technologies is highly relevant to government technology and mission priorities.

p. 2 · Read in context →

Jacobs Solutions Inc. (J)

A global engineering and technical-services firm that historically competed head-to-head with KBR in defense, space and intelligence before spinning that government business into Amentum in 2024; today the overlap sits in energy, environment and advanced-facilities engineering.

Jacobs describes the defense, space, intelligence and energy government-services business it spun off into Amentum in 2024 — a client base and scope that closely mirror KBR's Government Solutions.

Prior to the Separation Transaction, Jacobs' Critical Mission Solutions line of business provided a full spectrum of solutions for clients to address evolving challenges like digital transformation and modernization, national security and defense, space exploration, digital asset management, the clean energy transition, and nuclear decommissioning and cleanup. […] Clients included the U.S. Department of Defense (DoD), the Combatant Commands, the U.S. Intelligence Community, NASA, the U.S. Department of Energy (DoE)

p. 15 · Read in context →

Jacobs's FY2025 10-K names its own competitor set for engineering and consulting markets — several of them (Fluor, Bechtel, Parsons, AtkinsRealis) also rivals of KBR — but does not name KBR itself.

We compete with many companies across the world including technology, consulting and engineering firms. Typically, no single company or companies dominate the markets in which we provide services, and often we partner with our competitors or other companies to jointly pursue projects. […] Bechtel, Arup, Endava, Exponent, Mott MacDonald, Stantec, Parsons, Accenture, Mace, AtkinsRealis, Altair, Montrose, Capgemini, Fluor, Deloitte, KPMG, PwC, Bain & Company and McKinsey & Company are some of our competitors.

p. 12 · Read in context →

More peer documents

Amentum — FY2024 Form 10-K — FY2024 · 101 pages · Prior-year 10-K names the identical primary-competitor set including KBR Inc., confirming the KBR designation is recurring. · Open →

Leidos — Q4 FY2025 earnings call — Q4 FY2025 · 13 pages · CEO cites a 1.3x book-to-bill and 15% funded-backlog growth plus a large near-term pipeline — demand read-through for the government-services pool KBR bids into. · Open →

Leidos — Q1 FY2026 earnings call — Q1 FY2026 · 11 pages · Intelligence-community mission-support growth and Leidos's “trusted mission AI” strategy — the AI-for-government push that collides with KBR intelligence and IT modernization. · Open →

SAIC — Q1 FY2026 earnings call — Q1 FY2026 · 15 pages · Space Development Agency mission-integrator win and alignment to DoD priorities across space, missile defense and intelligence — direct space/defense collision with KBR. · Open →

Amentum — Q2 FY2026 earnings call — Q2 FY2026 · 9 pages · CEO sizes the combined addressable market as growing 10%+ annually across nuclear energy and space systems — the space/nuclear scope KBR also targets. · Open →

Technip Energies — FY2025 annual report — FY2025 · 392 pages · Current-year restatement of the hydrogen (30% installed base) and ethylene-licensing leadership claims, and lists KBR Inc. among its U.S. peer companies. · Open →

Booz Allen — Q3 FY2026 earnings call — Q3 FY2026 · 12 pages · Fullest read on the DOGE-era federal-efficiency environment (slower funding, thinned acquisition workforce) plus the exclusive a16z government technology partnership. · Open →

Jacobs — Q2 FY2026 earnings call — Q2 FY2026 · 11 pages · Record backlog, 1.4x book-to-bill, #1 ENR design-firm ranking and triple-digit data-center growth — Jacobs's momentum in the advanced-facilities/energy markets that overlap KBR. · Open →

Source: S&P Capital IQ consensus via Xpressfeed · Generated 2026-07-17.

Street snapshot

Seven analysts set a mean price target of USD 46.57 (median 45), spanning a wide 36 to 60 range.

Currency: USD · Scale: money in millions, absolute (per share) · Analyst counts shown explicitly; recommendation respondents: 8.

| Street view | Reading | Analysts |

|---|---|---|

| Recommendation mix | Buy 4, Outperform 0, Hold 4, Underperform 0, Sell 0 | 8 |

| Consensus score | 2.00 | 8 |

| Target price | mean 46.57; high 60.00; low 36.00 | 7 |

Forward table

Consensus frames low-single-digit revenue growth, from FY2025's actual USD 7,786m to roughly 7,982m, 8,411m and 8,696m across FY2026-FY2028, with gross margin holding near 16% and normalized EPS drifting from 3.93 to about 4.13. Coverage thins in the outer years, with revenue contributors falling from 11 in FY2025 to 3 by FY2028.

Currency: USD · Scale: money in millions, absolute (per share) · Analyst count is the estimate count for each period and metric.

| Period | Metric | Mean | YoY | Analysts | Low / high |

|---|---|---|---|---|---|

| FY0E | Revenue | 7,982 | 2.5% | 9 | 7,760 / 8,242 |

| FY0E | EBITDA | 999.4 | 3.2% | 9 | 966.2 / 1,020 |

| FY0E | EBIT | 807.6 | 4.9% | — | — / — |

| FY0E | Net income (GAAP) | 468.2 | 12.8% | 5 | 439.4 / 480.0 |

| FY0E | Net income (normalized) | 499.5 | 0.7% | — | — / — |

| FY0E | EPS (GAAP) | 3.69 | 15.1% | 5 | 3.50 / 3.79 |

| FY0E | EPS (normalized) | 3.96 | 0.8% | 9 | 3.83 / 4.05 |

| FY0E | Free cash flow | 399.0 | -32.4% | — | — / — |

| FY0E | Dividend per share | 0.67 | 0.9% | — | — / — |

| FY0E | Gross margin | 16.0% | 1.5% | — | — / — |

| FY0E | Capital expenditure | -44.85 | 33.7% | — | — / — |

| FY0E | Net debt | 1,916 | -7.1% | — | — / — |

| FY0E | Cash from operations | 511.0 | -8.8% | — | — / — |

| FY0E | ROE | 30.3% | -6.9% | — | — / — |

| FY+1E | Revenue | 8,411 | 5.4% | 9 | 8,110 / 8,625 |

| FY+1E | EBITDA | 1,009 | 0.9% | 9 | 941.9 / 1,097 |

| FY+1E | EBIT | 825.5 | 2.2% | — | — / — |

| FY+1E | Net income (GAAP) | 493.4 | 5.4% | 5 | 443.9 / 558.0 |

| FY+1E | Net income (normalized) | 506.9 | 1.5% | — | — / — |

| FY+1E | EPS (GAAP) | 3.92 | 6.2% | 5 | 3.67 / 4.39 |

| FY+1E | EPS (normalized) | 4.13 | 4.2% | 9 | 3.77 / 4.59 |

| FY+1E | Free cash flow | 554.2 | 38.9% | — | — / — |

| FY+1E | Dividend per share | 0.72 | 8.1% | — | — / — |

| FY+1E | Gross margin | 15.8% | -1.1% | — | — / — |

| FY+1E | Capital expenditure | -46.87 | 4.5% | — | — / — |

| FY+1E | Net debt | 1,582 | -17.4% | — | — / — |

| FY+1E | Cash from operations | 482.4 | -5.6% | — | — / — |

| FY+1E | ROE | 25.8% | -14.8% | — | — / — |

| FY+2E | Revenue | 8,696 | 3.4% | 3 | 8,179 / 8,993 |

| FY+2E | EBITDA | 969.1 | -3.9% | 3 | 908.0 / 1,024 |

| FY+2E | EBIT | 794.3 | -3.8% | — | — / — |

| FY+2E | Net income (GAAP) | 457.9 | -7.2% | 2 | 422.7 / 493.1 |

| FY+2E | Net income (normalized) | 497.5 | -1.8% | — | — / — |

| FY+2E | EPS (GAAP) | 3.82 | -2.7% | 2 | 3.63 / 4.01 |

| FY+2E | EPS (normalized) | 4.13 | 0.1% | 3 | 3.88 / 4.27 |

| FY+2E | Dividend per share | 0.75 | 4.2% | — | — / — |

| FY+2E | Gross margin | 16.1% | 1.7% | — | — / — |

| FY+2E | Capital expenditure | -85.54 | 82.5% | — | — / — |

| FY+2E | Net debt | 1,214 | -23.2% | — | — / — |

| FY+2E | ROE | 23.0% | -10.8% | — | — / — |

| Q2 FY2026 | Revenue | 1,869 | -4.3% | 8 | 1,742 / 1,939 |

| Q2 FY2026 | EBITDA | 230.8 | -4.6% | 8 | 215.8 / 250.2 |

| Q2 FY2026 | EBIT | 188.4 | -3.1% | — | — / — |

| Q2 FY2026 | Net income (GAAP) | 111.4 | 52.6% | 5 | 101.3 / 121.8 |

| Q2 FY2026 | Net income (normalized) | 114.6 | -2.8% | — | — / — |

| Q2 FY2026 | EPS (GAAP) | 0.88 | 56.4% | 5 | 0.80 / 0.95 |

| Q2 FY2026 | EPS (normalized) | 0.90 | -0.7% | 8 | 0.85 / 1.00 |

| Q2 FY2026 | Dividend per share | 0.17 | -1.0% | — | — / — |

| Q2 FY2026 | Gross margin | 16.1% | 7.1% | — | — / — |

| Q2 FY2026 | Capital expenditure | -10.16 | -33.6% | — | — / — |

| Q2 FY2026 | ROE | 28.5% | -12.7% | — | — / — |

| Q3 FY2026 | Revenue | 2,058 | 6.6% | 8 | 1,966 / 2,127 |

| Q3 FY2026 | EBITDA | 256.2 | 6.7% | 8 | 238.0 / 272.9 |

| Q3 FY2026 | EBIT | 212.0 | 8.1% | — | — / — |

| Q3 FY2026 | Net income (GAAP) | 125.6 | 9.2% | 5 | 111.0 / 135.9 |

| Q3 FY2026 | Net income (normalized) | 131.1 | 7.4% | — | — / — |

| Q3 FY2026 | EPS (GAAP) | 0.99 | 10.3% | 5 | 0.89 / 1.08 |

| Q3 FY2026 | EPS (normalized) | 1.03 | 1.1% | 8 | 0.95 / 1.13 |

| Q3 FY2026 | Dividend per share | 0.17 | -1.0% | — | — / — |

| Q3 FY2026 | Gross margin | 16.3% | 4.3% | — | — / — |

| Q3 FY2026 | Capital expenditure | -11.06 | 24.0% | — | — / — |

| Q3 FY2026 | ROE | 33.6% | 4.5% | — | — / — |

| Q4 FY2026 | Revenue | 2,100 | 11.4% | 8 | 2,001 / 2,204 |

| Q4 FY2026 | EBITDA | 260.0 | 9.2% | 8 | 242.5 / 271.6 |

| Q4 FY2026 | EBIT | 214.2 | 7.3% | — | — / — |

| Q4 FY2026 | Net income (GAAP) | 126.9 | 14.3% | 5 | 116.2 / 139.0 |

| Q4 FY2026 | Net income (normalized) | 133.7 | 9.7% | — | — / — |

| Q4 FY2026 | EPS (GAAP) | 1.01 | 15.6% | 5 | 0.91 / 1.10 |

| Q4 FY2026 | EPS (normalized) | 1.06 | 6.6% | 8 | 0.95 / 1.12 |

| Q4 FY2026 | Dividend per share | 0.17 | -1.0% | — | — / — |

| Q4 FY2026 | Gross margin | 16.3% | -1.0% | — | — / — |

| Q4 FY2026 | Capital expenditure | -11.47 | 51.4% | — | — / — |

| Q4 FY2026 | ROE | 30.9% | -2.2% | — | — / — |

| Q1 FY2027 | Revenue | 2,060 | 7.1% | 5 | 2,006 / 2,115 |

| Q1 FY2027 | EBITDA | 263.4 | 5.0% | 5 | 248.0 / 270.3 |

| Q1 FY2027 | EBIT | 222.4 | 18.1% | — | — / — |

| Q1 FY2027 | Net income (GAAP) | 131.7 | 29.2% | 3 | 125.0 / 136.1 |

| Q1 FY2027 | Net income (normalized) | 137.7 | 19.8% | — | — / — |

| Q1 FY2027 | EPS (GAAP) | 1.05 | 31.3% | 3 | 0.98 / 1.09 |

| Q1 FY2027 | EPS (normalized) | 1.10 | 14.8% | 5 | 0.98 / 1.15 |

| Q1 FY2027 | Dividend per share | 0.20 | 18.2% | — | — / — |

| Q1 FY2027 | Gross margin | 17.2% | 7.0% | — | — / — |

| Q1 FY2027 | Capital expenditure | -11.66 | 16.0% | — | — / — |

| Q1 FY2027 | ROE | 30.9% | -0.5% | — | — / — |

Estimate momentum

FY2027 estimates have edged lower over the past six months, revenue easing from about 8,582m (180 days ago) to 8,411m and normalized EPS from 4.34 to 4.13. The FY2028 cuts are larger — normalized EPS from 6.37 to 4.13 — but rest on only three estimates, so the signal is weak.

Currency: USD · Scale: money in millions, absolute (per share) · Point-in-time consensus; analyst count is shown where supplied.

| Period | Metric | Lookback | Then | Now | Direction / magnitude | Analysts |

|---|---|---|---|---|---|---|

| 2027 | EPS (normalized) | 30d | 4.15 | 4.13 | down 0.5% | — |

| 2027 | EPS (normalized) | 90d | 4.20 | 4.13 | down 1.6% | — |

| 2027 | EPS (normalized) | 180d | 4.34 | 4.13 | down 4.9% | — |

| 2027 | Revenue | 30d | 8,411 | 8,411 | up 0.0% | — |

| 2027 | Revenue | 90d | 8,453 | 8,411 | down 0.5% | — |

| 2027 | Revenue | 180d | 8,582 | 8,411 | down 2.0% | — |

| 2028 | Revenue | 30d | 8,696 | 8,696 | flat 0.0% | — |

| 2028 | Revenue | 90d | 8,889 | 8,696 | down 2.2% | — |

| 2028 | Revenue | 180d | 9,852 | 8,696 | down 11.7% | — |

| 2028 | EPS (normalized) | 30d | 4.13 | 4.13 | flat 0.0% | — |

| 2028 | EPS (normalized) | 90d | 4.70 | 4.13 | down 12.1% | — |

| 2028 | EPS (normalized) | 180d | 6.37 | 4.13 | down 35.1% | — |

Beat / miss record

Current sequences by metric: Revenue: 1 consecutive beat; EPS (normalized): 6 consecutive beats.

Currency: USD · Scale: money in millions, absolute (per share) · Consensus is captured before each actual first became effective; analyst count shown per observation.

| Quarter | Metric | Consensus as of | Actual | Surprise | Outcome | Analysts |

|---|---|---|---|---|---|---|

| Q1 FY2026 | Revenue | 1,877 | 1,923 | 2.4% | Beat | — |

| Q1 FY2026 | EPS (normalized) | 0.91 | 0.96 | 5.5% | Beat | — |

| Q4 FY2025 | Revenue | 1,905 | 1,885 | -1.1% | Miss | — |

| Q4 FY2025 | EPS (normalized) | 0.95 | 0.99 | 4.4% | Beat | — |

| Q3 FY2025 | Revenue | 1,973 | 1,931 | -2.1% | Miss | — |

| Q3 FY2025 | EPS (normalized) | 0.95 | 1.02 | 6.9% | Beat | — |

| Q2 FY2025 | Revenue | 2,081 | 1,952 | -6.2% | Miss | — |

| Q2 FY2025 | EPS (normalized) | 0.88 | 0.91 | 3.0% | Beat | — |

| Q1 FY2025 | Revenue | 2,072 | 2,055 | -0.8% | Miss | — |

| Q1 FY2025 | EPS (normalized) | 0.86 | 0.98 | 13.7% | Beat | — |

| Q4 FY2024 | Revenue | 1,999 | 2,122 | 6.2% | Beat | — |

| Q4 FY2024 | EPS (normalized) | 0.82 | 0.91 | 11.4% | Beat | — |

| Q3 FY2024 | Revenue | 1,959 | 1,947 | -0.6% | Miss | — |

| Q3 FY2024 | EPS (normalized) | 0.84 | 0.84 | -0.0% | Miss | — |

| Q2 FY2024 | Revenue | 1,876 | 1,855 | -1.1% | Miss | — |

| Q2 FY2024 | EPS (normalized) | 0.79 | 0.83 | 4.7% | Beat | — |

Where the street disagrees

Disagreement concentrates in the outer years, where coverage falls to a handful of analysts: FY2028 revenue carries a USD 367m standard deviation across just three estimates, and its GAAP net income rests on only two. Near-term lines are markedly tighter.

Currency: USD · Scale: money in millions, absolute (per share) · Dispersion is high-low divided by absolute mean; analyst count shown per item.

| Period | Metric | Mean | Low | High | Spread / mean | Analysts |

|---|---|---|---|---|---|---|

| Q3 FY2025 | Net income (GAAP) | 106.2 | 81.31 | 116.0 | 32.7% | 4 |

| Q3 FY2025 | EPS (GAAP) | 0.82 | 0.63 | 0.89 | 31.4% | 4 |

| 2027 | Net income (GAAP) | 493.4 | 443.9 | 558.0 | 23.1% | 5 |

| Q2 FY2025 | EPS (normalized) | 0.88 | 0.80 | 0.99 | 21.5% | 6 |

| Q2 FY2025 | Net income (GAAP) | 110.5 | 100.0 | 123.0 | 20.8% | 4 |

Source: S&P Capital IQ transcripts via Xpressfeed · latest indexed call 2026-05-05 · generated 2026-07-17.

Latest call digest

KBR, Inc., Q1 2026 Earnings Call, May 05, 2026 · 2026-05-05T12:30:00

KBR's Q1 2026 call (May 5, 2026) was a reaffirm-and-reassure quarter. Prepared remarks led with resilience: adjusted EBITDA margin expanded to 13.1% from 12.3%, adjusted operating cash flow was $119 million, and adjusted EPS was $0.96 (down $0.05 year-over-year). Management reaffirmed full-year 2026 guidance across all metrics and stressed visibility — work under contract covers roughly 67% of 2026 STS revenue guidance and 91% of MTS. Sustainable Tech again carried the bookings story: STS book-to-bill ex LNG of 1.2x, its third consecutive quarter above 1.0, with backlog of about $4.7 billion, up 9% year-over-year. Mission Tech was framed more cautiously — book-to-bill of 1.0, backlog and options of $18.5 billion, and $16 billion of bids awaiting award, with awards "not flowing at historical levels."

Two prepared-remarks items reset expectations. First, the spin of Mission Tech moved to an effective date of January 4, 2027, from the "second half of 2026" targeted a quarter earlier, with public Form 10 filing now expected in September and Investor Days in the second week of November. Second, management flagged a new NASA in-sourcing directive that could shift some contractor work back to government payroll; Stuart Bradie sized the gross impact at roughly $50 million to $60 million this year and said it would likely be less, offset by Sustainable Tech strength so full-year guidance holds on mix, not level.

The Q&A reality was tougher than the script. Analysts pressed on why the 13.1% margin ran ahead of the full-year guide, whether the STS margin ex LNG really builds toward 20%-plus (management held to a ~15%-and-rising base), and why the spin now looks behind schedule. Management declined to raise guidance despite a strong start — Bradie said getting "out over your skis" would not be prudent — and repeatedly deferred stand-alone economics and multi-year growth to the November Investor Days.

Participant coverage from the latest call.

| Group | Participants | Count |

|---|---|---|

| Management | Operator; Rachael Goldwait — Vice President of Investor Relations, KBR, Inc.; Stuart Bradie — CEO, President & Chairman, KBR, Inc.; Shad Evans — Executive VP & Chief Financial Officer, KBR, Inc. | 4 |

| Analysts | Adam Bubes — Research Analyst, Goldman Sachs Group, Inc., Research Division; Unknown Analyst; Jerry Revich — Equity Analyst, Wells Fargo Securities, LLC, Research Division; Ian Zaffino — MD & Senior Analyst, Oppenheimer & Co. Inc., Research Division; Mariana Perez Mora — Research Analyst, BofA Securities, Research Division; Tobey Sommer — Managing Director, Truist Securities, Inc., Research Division; Steven Fisher — Executive Director & Senior Analyst, UBS Investment Bank, Research Division | 7 |

Curated latest-call exchanges; one row per analyst topic.

| Analyst | Firm | Topic | What changed in Q&A |

|---|---|---|---|

| Adam Bubes | Goldman Sachs | Q1 margin beat and equity income | Asked what drove the 13.1% margin above the full-year guide; CFO tied it to long-term targets and continued LNG-project contribution into early 2027. |

| Unknown Analyst (for Andrew Kaplowitz) | Citi | STS margin ex LNG | Pressed on the underlying STS margin path versus the 20%-plus framework; management set the base business near 15% ex LNG and rising, driven by technology and JV OpEx mix. |

| Jerry Revich | Wells Fargo | NASA in-sourcing and LNG backfill | Management quantified the NASA in-sourcing headwind at roughly $50-60 million gross this year, likely less, and expressed confidence in backfilling the rolling-off LNG project through STS bookings momentum. |

| Ian Zaffino | Oppenheimer | Middle East bookings and spin timing | Questioned why the spin looks behind schedule; management framed the January 4, 2027 date as fiscal-year alignment plus schedule float for IT separation, not a problem signal. |

| Mariana Perez Mora | BofA | STS closeout size and multi-year growth | Management declined to size the STS project closeout and deferred the two-to-three-year growth trajectory to the Investor Days. |

| Steven Fisher | UBS | Guidance raise and STS project maturity | Management declined to raise guidance despite a beat, citing macro volatility, and characterized the STS pipeline as maturing projects rather than early-stage concepts. |

Theme tracker

Themes are curator-classified across supplied calls.

| Theme | Status | Quarters mentioned | Read-through |

|---|---|---|---|

| Mission Tech spin-off | emerged | Q3 2025, Q4 2025, Q1 2026 | Announced September 24, 2025 and central to every call since; the target has drifted from "mid- to late 2026" to an effective date of January 4, 2027, and stand-alone economics keep being deferred to Investor Days. |

| HomeSafe program | dropped | Q2 2024, Q3 2024, Q4 2024, Q1 2025, Q2 2025 | A recurring growth pillar for roughly two years; TRANSCOM terminated the contract in Q2 2025 and it has been absent from the last three calls, so its disappearance reflects a real lost program rather than de-emphasis. |

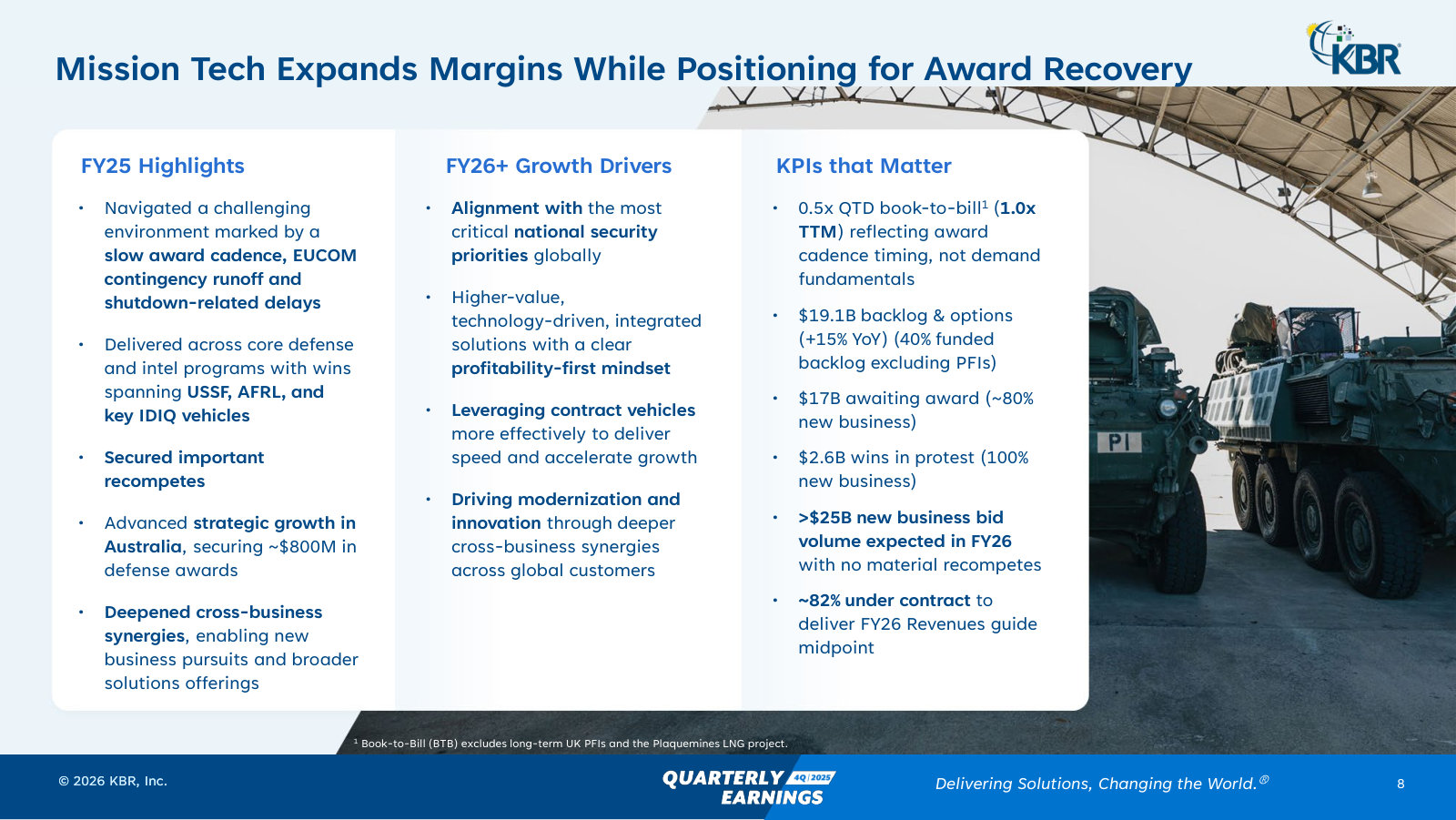

| MTS award delays and protests | persisted | Q1 2025, Q2 2025, Q4 2025, Q1 2026 | Protest activity and slow award cadence have weighed on Mission Tech revenue for several quarters, with roughly $2 billion in awards stuck in protest through 2025 and the MIST contract cited most recently. |

| NASA funding and in-sourcing uncertainty | persisted | Q2 2025, Q3 2025, Q4 2025, Q1 2026 | NASA budget risk has recurred, evolving from broad appropriations uncertainty into a specific in-sourcing directive in Q1 2026 that management sized at roughly $50-60 million gross this year. |

| LNG project margin and backfill | persisted | Q4 2024, Q2 2025, Q4 2025, Q1 2026 | The consolidated LNG project has been a repeated STS margin tailwind; the debate has shifted to how the portfolio backfills the ~500 basis points it contributes as it rolls off into 2027. |

| EUCOM contingency roll-off | persisted | Q2 2025, Q3 2025, Q4 2025, Q1 2026 | The planned wind-down of EUCOM/Ukraine contingency work is a recurring year-over-year revenue headwind that management flags as low-margin and largely anticipated. |

Guidance ledger

Quotes, calls, and speakers are source-verified; outcomes are curator-classified.

| Verbatim guidance | Call | Speaker | Curator outcome | Outcome note |

|---|---|---|---|---|

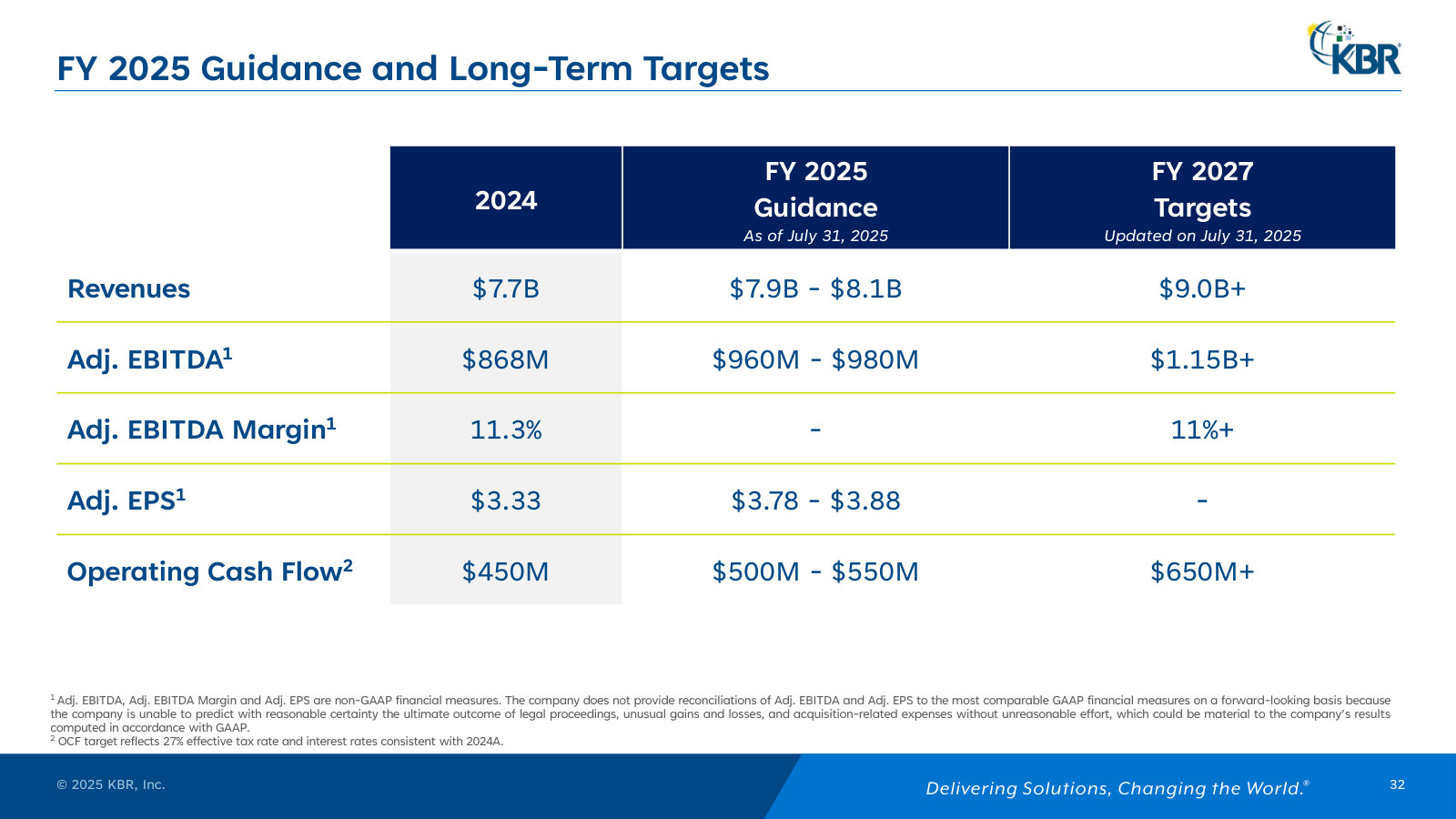

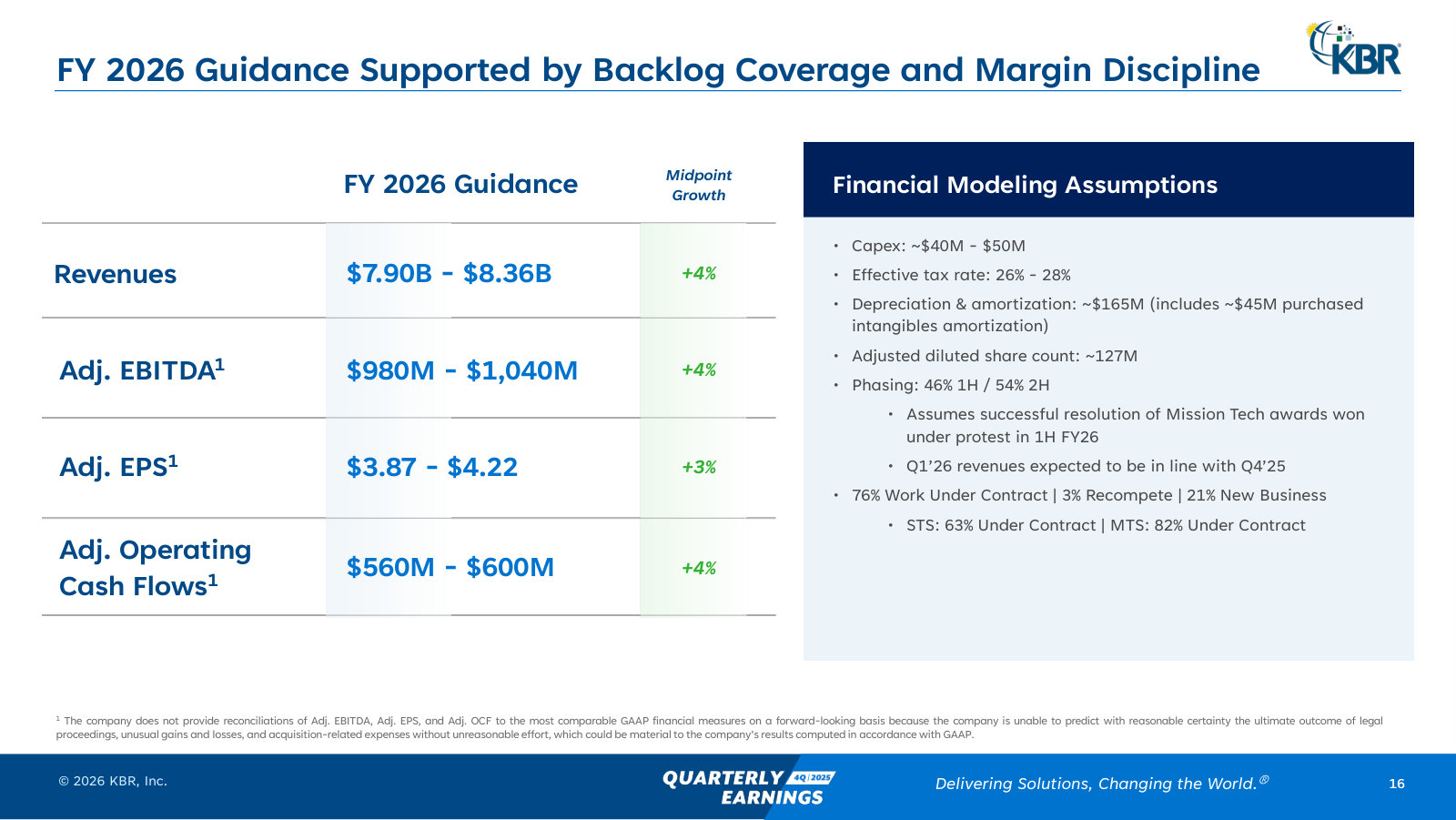

| “we are guiding revenues in the range of $7.9 billion to $8.36 billion, adjusted EBITDA of $980 million to $1.04 billion, adjusted EPS of $3.87 to $4.22 and adjusted operating cash flow of $560 million to $600 million.” | KBR, Inc., Q4 2025 Earnings Call, Feb 26, 2026 · 2026-02-26T13:30:00 | Shad Evans | pending | Reaffirmed across all metrics on the Q1 2026 call; full-year outcome not yet resolved in the supplied history. |

| “We expect to bid more than $25 billion in 2026, and that will be up double digits year-over-year.” | KBR, Inc., Q4 2025 Earnings Call, Feb 26, 2026 · 2026-02-26T13:30:00 | Stuart Bradie | pending | On the Q1 2026 call management said it continues to make progress toward the $25 billion bid-volume goal, with significant submissions expected in the next two quarters. |

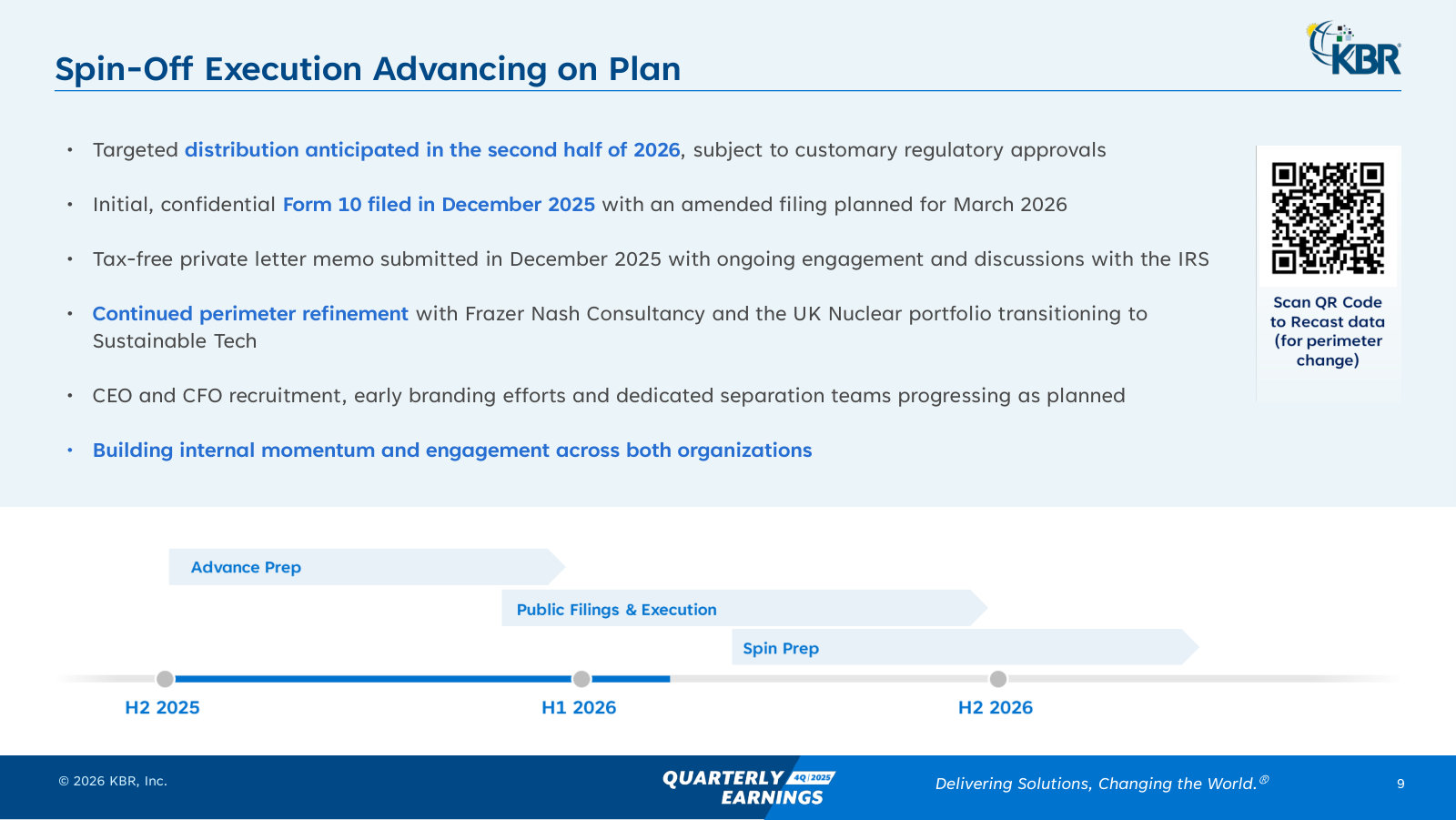

| “our targeted distribution is anticipated in the second half of 2026.” | KBR, Inc., Q4 2025 Earnings Call, Feb 26, 2026 · 2026-02-26T13:30:00 | Stuart Bradie | missed | On the Q1 2026 call the spin was moved to an effective date of January 4, 2027, pushing the distribution out of the second half of 2026. |

| “we expect revenue in the range of $8.7 billion to $9.1 billion, representing an increase of 15% at the midpoint.” | KBR, Inc., Q4 2024 Earnings Call, Feb 24, 2025 · 2025-02-24T21:00:00 | Mark Sopp | missed | Revenue guidance was cut to $7.9-8.1 billion in Q2 2025 after the HomeSafe termination; the Q4 2025 call reported full-year 2025 revenue of approximately $7.8 billion. |

| “Our estimated revenue range is $300 million to $500 million for the year.” | KBR, Inc., Q4 2024 Earnings Call, Feb 24, 2025 · 2025-02-24T21:00:00 | Mark Sopp | missed | This HomeSafe revenue assumption was removed after TRANSCOM terminated the HomeSafe contract, disclosed on the Q2 2025 call. |

Q&A pressure map

Question counts and firms are curator tallies; analyst coverage shown above.

| Topic | Questions | Firms | Pressure / response |

|---|---|---|---|

| STS margin structure ex LNG | 3 | Goldman Sachs, Citi | The most-pressed topic on the Q1 2026 call: analysts probed why the reported margin ran ahead of guide and whether the base business really builds toward 20%-plus once the LNG project rolls off. |

| NASA in-sourcing exposure | 2 | Wells Fargo, Truist | Analysts pushed on the size and timing of the NASA in-sourcing directive; management answered directly, sizing it at roughly $50-60 million gross and noting it affects mainly one contract. |

| Spin timing and portfolio | 2 | Oppenheimer, BofA | On the Q1 2026 call analysts asked why the spin looks behind schedule and whether parts of MTS could be sold; management defended the January 2027 date as fiscal-year alignment and said it would weigh any offer on shareholder value. |

| STS pipeline and LNG backfill | 2 | Wells Fargo, UBS | Analysts pressed on how much visibility supports replacing the LNG project and how mature the STS pipeline is; management pointed to a third straight strong bookings quarter and front-end work on three LNG projects. |

| Guidance upside and multi-year growth | 2 | UBS, BofA | Requests to lean toward the upper end of guidance and to frame two-to-three-year growth were deflected — the first citing macro volatility, the second deferred to the November Investor Days. |

Language shifts

Only language evidence verified against the referenced component is shown.

| Observation | Verbatim evidence | Call ID | Component |

|---|---|---|---|

| Management introduced explicit wider-outcome caution around the government portfolio when reaffirming 2026 guidance, framing the range of results as unusually broad. | “the range of potential outcomes is wider than normal for our Government Services portfolio.” | 1993638985 | 3 |

| Management continued to describe the Mission Tech award backdrop in subdued terms, a caution that has persisted through the soft-award cycle. | “awards are not flowing at historical levels.” | 1993638985 | 2 |

| In the closing remarks, management characterized the near-term Mission Tech award environment as uneven, a measured tone versus the growth framing of earlier years. | “the near-term award environment remains uneven. It's a good way to describe it.” | 1993638985 | 44 |

| On guidance, management leaned on colloquial caution to explain why it would not raise after a strong start, signaling deliberate conservatism amid macro volatility. | “to get out over your skis right now would not generally be viewed positively” | 1993638985 | 40 |

The call history shows a company managing through a soft government-award cycle — protests, EUCOM roll-off and now a NASA in-sourcing directive — while Sustainable Tech bookings strengthen and the Mission Tech spin advances. With the spin slipped to January 2027 and stand-alone economics repeatedly deferred to the November Investor Days, the central question of each business's independent earnings power stays unresolved for now.

KBR: the business, the record, and the question

KBR is a $7.8 billion-revenue provider of engineering, technical and mission services, split between government programs and licensed process technology. Over four years operating margins roughly doubled and adjusted earnings kept beating estimates, yet the stock trades near $35 — about 40% below its late-2024 high and roughly nine times forward earnings. This report exists to test whether that de-rating misprices a structurally better business or fairly prices a government-dependent contractor.

What KBR is

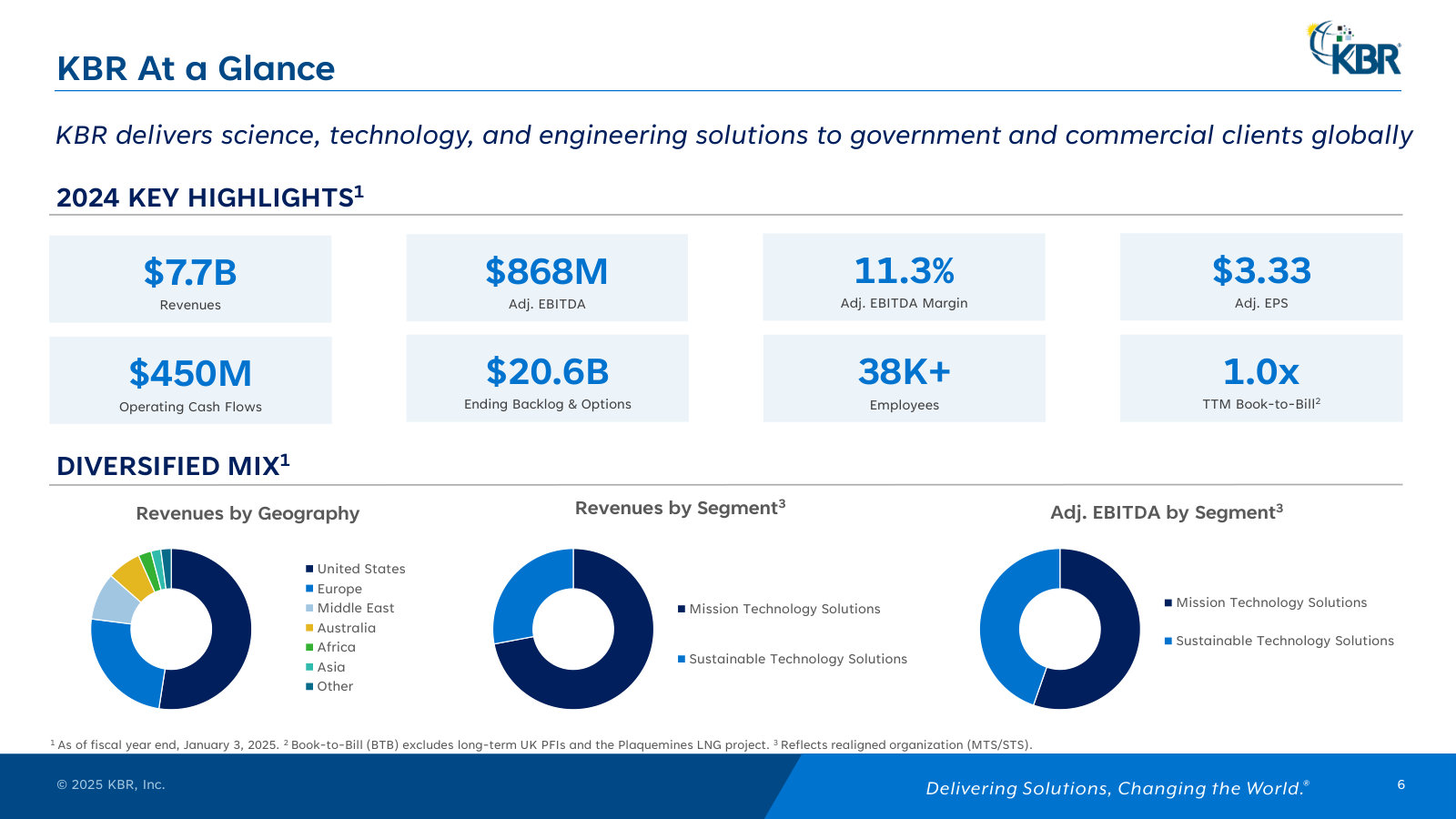

KBR, Inc. (NYSE: KBR) is a Houston-based descendant of Kellogg Brown & Root, spun out of Halliburton and public since 2006. It no longer builds the large energy-and-construction projects that once defined it. Today it sells knowledge work — engineering, systems integration, program management, data analytics — plus a portfolio of patented industrial process technologies. The business is organized into two core segments [1]:

- Mission Technology Solutions (MTS) — full life-cycle support to defense, intelligence, space and aviation programs for the U.S., U.K. and Australian governments, spanning research, prototyping, systems engineering, C5ISR, cyber and program management [2]. At $5.6 billion of FY2025 revenue, MTS is roughly 72% of the company.

- Sustainable Technology Solutions (STS) — a portfolio of over 85 proprietary, sustainability-focused process technologies (ammonia/syngas, chemicals/petrochemicals, clean refining, circular economy) that KBR licenses, along with proprietary equipment, catalysts and high-end engineering and advisory work [3]. At $2.2 billion, STS is about 28% of revenue — but, as the segment economics below show, a much larger share of the profit.

Revenue (FY2025)

Operating Income

Net Income (to KBR)

Backlog

Market Cap

Forward P/E

Revenue, operating income, net income and backlog: FY2025 Form 10-K (year ended Jan 2, 2026) [4], backlog p.20 [5]. Market cap and forward P/E derived from the $35.17 close on Jul 17, 2026, ~129M shares, and consensus estimates.

KBR labels the year ended January 2, 2026 as fiscal 2025; its 52/53-week calendar means fiscal years end in late December or early January. All figures here follow that convention.

How it makes money

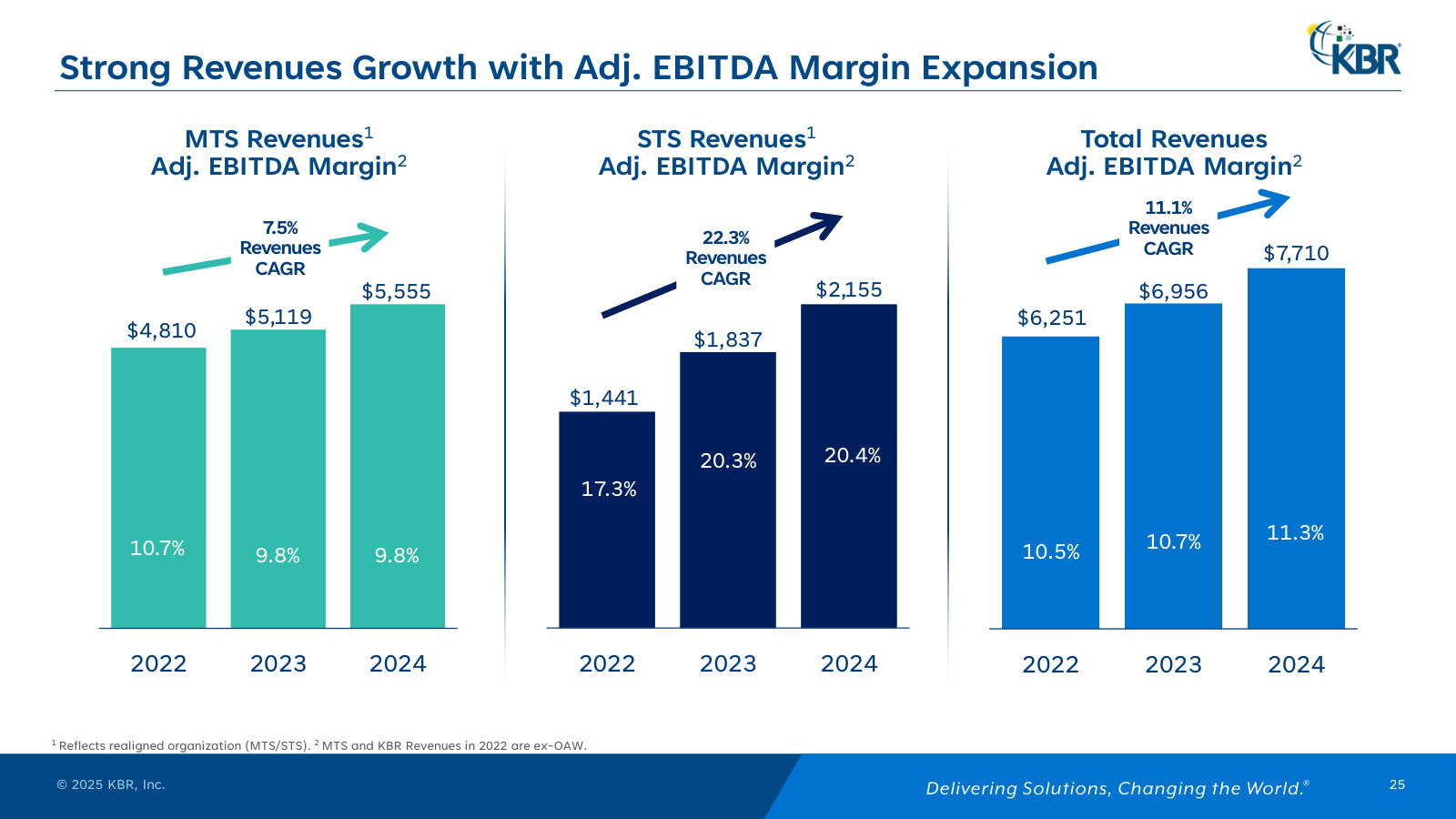

The two segments earn their profit very differently, and this is the first thing a new reader should internalize. MTS is the scale engine — large, recurring, mostly cost-reimbursable and fixed-price government contracts that turn over slowly and carry single-digit margins. STS is the profit engine — licensing and proprietary technology that carry more than double the operating margin. In FY2025, STS produced slightly more segment operating income than MTS on less than half the revenue.

Source: FY2025 Form 10-K, Results of Operations by Business Segment [6]. Corporate expense of $162M (not shown) reconciles segment income to the $778M consolidated operating figure.

Two structural features follow from this mix. First, KBR's profitability is more sensitive to STS — the smaller, higher-margin, more cyclical, energy-and-chemicals-exposed segment — than its revenue split suggests. Second, a meaningful slice of profit sits outside consolidated operations: FY2025 operating income included $210 million of equity in earnings of unconsolidated joint ventures, nearly double the prior year, and about 17% of backlog is work executed through equity-method JVs [7]. How readily that JV profit converts to KBR cash is a question later chapters should press.

The financial record

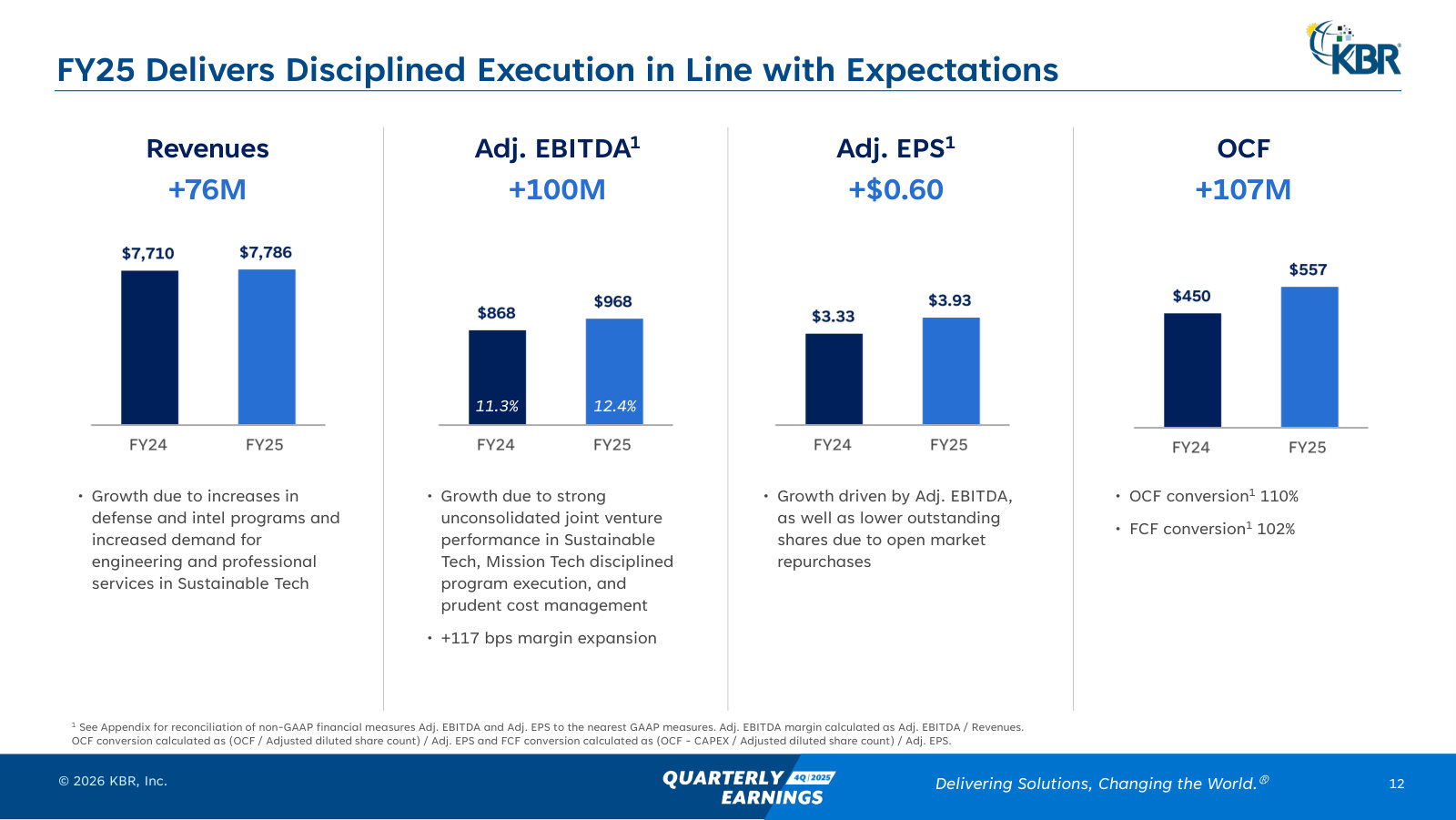

The reported numbers describe a business that has grown revenue and expanded margin steadily since 2022. Operating income rose from $343 million to $778 million over three years, lifting the operating margin from roughly 5% to 10% [8].

Source: FY2023 and FY2025 Forms 10-K, Consolidated Statements of Operations [9].

The one blemish in that record is FY2023, when KBR reported a net loss of $265 million. It is worth being precise about why, because the headline reads worse than the year was. The loss did not come from operations — operating income that year was still a positive $449 million. It came almost entirely from two below-the-line, largely one-time items: a $494 million charge to settle its Convertible Notes, and a $144 million charge (recorded within operating income) to settle a legacy legal matter [10]. The convertible charge was the swing factor that turned a profitable operating year into a reported loss.

Source: FY2023 figures per the FY2025 Form 10-K, Consolidated Statements of Operations [11]. Operating income already reflects the $144M legal settlement charge.

That episode matters twice over. It explains why a screen for "companies that lost money three years ago" flags KBR misleadingly. And it is a reminder that KBR's reported and adjusted numbers can diverge: even in the clean year FY2025, reported diluted EPS of $3.21 sat below the $3.49 earned by continuing operations, because a $55 million loss from discontinued operations — chiefly the terminated HomeSafe military-moving contract — dragged the total down [12]. The gap between what KBR earns operationally and what it reports on a GAAP basis is a theme this report will return to.

The de-rating

For a reader meeting KBR for the first time, the price chart is the reason the name is interesting now. The stock re-rated sharply from 2019 through 2024 as investors rewarded its pivot into defense, space and energy-transition markets, peaking near $58 at the end of 2024. It has since fallen to about $35 — a decline of roughly 40% — even as backlog, margins and adjusted earnings continued to rise.

Source: year-end closing share prices; 2026 value is the Jul 17, 2026 close, as reported.

What changed in 2025 was sentiment, not results. Two overhangs dominate. First, government-spending risk moved to the front page: on January 20, 2025 an executive order created the DOGE cost-cutting commission, and although it was disbanded in November 2025, the episode crystallized how exposed KBR is — U.S. government revenue was 57% of the FY2025 total [13]. Second, in June 2025 the U.S. Transportation Command abruptly terminated HomeSafe's role in the Global Household Goods Contract — a marquee win that KBR then moved to discontinued operations [14]. Against that, the operating business kept beating: reported quarterly EPS has topped consensus in every quarter of the last two years.

At $35, KBR trades near 11 times trailing GAAP earnings and roughly nine times consensus forward earnings of about $3.96, against a mean analyst target near $47. That is a valuation set well below the market multiple — the profile of a company the market has stopped paying up for, not one it has priced for growth.

Durability of the balance sheet

Because the de-rating invites the question of whether cheapness signals distress, the balance sheet deserves a first look here. It does not read as distressed. KBR carries about $2.6 billion of debt against $0.5 billion of cash, for net debt near $2.1 billion — roughly 2.2 times EBITDA — and generated $410 million of free cash flow in FY2025 [15]. The clearest balance-sheet caveat is that $2.7 billion of goodwill exceeds the $1.5 billion of shareholders' equity, so tangible book value is negative — a consequence of an acquisition-led strategy rather than a solvency signal, but a reason a careful reader will want the cash-conversion and covenant picture examined in detail later.

Net Debt

Net Debt / EBITDA

Free Cash Flow (FY2025)

U.S. Gov't % of Revenue

Sources: net debt and free cash flow derived from the FY2025 Form 10-K statements [16]; U.S. government revenue share p.31 [17].

The question this report answers

KBR presents as a "fallen star": a name the market prized for its growth pivot and now discounts, trading below the broad market's multiple despite a rising order book and consistent earnings beats. That framing fits some of this investor's preferences and fails others — the valuation is undemanding and the balance sheet is not distressed, but KBR is not founder-run, and its fortunes are tied to U.S. government budgets rather than to a controlling owner with skin in the game.

The through-line for the chapters that follow is a single question:

Does KBR's roughly 40% de-rating since late 2024 misprice a structurally improved, backlog-backed business — one earning most of its profit from higher-margin licensed technology and mission-critical government work, with a $16.9 billion order book and consistent earnings beats — or does it fairly price a contractor that draws 57% of revenue from U.S. government budgets, reports GAAP profits and cash below its adjusted headline numbers, and answers to no controlling owner?

Answering it means separating the durable from the cyclical in the earnings, testing how much of the reported profit becomes cash, judging whether the government and energy-transition tailwinds are real, and gauging how much pessimism the price already embeds. Those are the chapters to come.

Earnings to Cash

KBR's reported profit turns into cash cleanly. In the year ended January 2, 2026, operating cash flow of $557 million and free cash flow of $515 million both exceeded not only GAAP net income of $403 million but management's own adjusted earnings of $507 million [1] [2]. The cash-conversion worry a skeptic raises first does not hold up. The earnings-quality question lives elsewhere: nearly half of continuing profit now comes from joint ventures KBR does not consolidate, and that contribution has swung from an $80 million loss to a $210 million gain in three years.

A note on labels: KBR's 52/53-week calendar means its most recent year ended January 2, 2026. This chapter calls it FY2025, matching how KBR and the SEC label it.

Cash runs ahead of the accounting profit

The clean test of earnings quality is whether reported profit becomes cash. Across the last three years — restated onto a continuing-operations basis in the latest 10-K — it does, with room to spare [3].

Source: FY2025 Annual Report (Form 10-K), Consolidated Statements of Cash Flows; free cash flow derived as operating cash flow less capital expenditures [4].

Operating cash flow rose from $301 million to $557 million over the three years, and free cash flow — after capital spending that runs just $42–62 million a year, or under 1% of revenue — climbed from $239 million to $515 million [5]. FY2023's net loss was the $494 million convertible-notes charge working below the operating line, a non-cash item added straight back in the cash-flow statement [6]; the business generated cash that year regardless.

Source: derived from FY2025 Annual Report (Form 10-K), Consolidated Statements of Cash Flows [7].

Cash conversion above 1.0x is not an accident of one year. It holds because depreciation and amortization ($169 million in FY2025) runs well ahead of the trivial capital budget, and because working capital has been broadly neutral: contract assets moved just $3 million in FY2025 and receivables $2 million, against $7.8 billion of revenue [8]. For a cost-plus and services book, that is what a healthy pattern looks like: no receivables build outrunning sales, no contract-asset balloon signalling revenue booked ahead of billing.

The adjusted-to-GAAP gap is small and legible

KBR's headline is an adjusted number, and the through-line notes that GAAP sits below it. It does — but the gap is modest and its parts are identifiable, not a euphemism for recurring costs dressed up as one-offs.

Source: Q4/Full-Year FY2025 Earnings Presentation, Adjusted EPS reconciliation [9].

The $0.72 distance from GAAP diluted EPS of $3.21 to adjusted EPS of $3.93 splits three ways: $0.28 is the discontinued-operations loss on winding down the HomeSafe military-moving contract; $0.28 is amortization of acquired intangibles; and $0.16 is spin-off, acquisition and integration cost [10]. Two of those three are real economic charges — the HomeSafe exit cost real money, and acquisition amortization is a genuine non-cash expense that recurs at roughly $57–58 million a year for the next five years as prior deals wash through [11]. An investor should treat adjusted EPS as the operating run-rate but not forget those costs exist.